Future of Mobile Money for Cocoa Farmers in Côte d’Ivoire, Ghana

Cocoa farmers in Côte d’Ivoire and Ghana produce close to 70% of the world’s cocoa, and they do it with mobile phones in their pockets.

That’s why the World Cocoa Foundation (WCF) launched a study in August 2015 with research partner Strategic Impact Advisors (SIA) to better understand the potential of mobile money to enhance farmers’ livelihoods. The research illuminates enormous potential for greater mobile money use by the cocoa farming population in both countries, where competitive mobile money offerings, conducive regulatory environments and expanding agent networks are already in place. Yet major adoption challenges persist.

The primary research delivers data and analysis of the awareness, use and interest in mobile money of 522 cocoa farmers in Côte d’Ivoire and Ghana – 220 farmers in six villages in the Sud Comoe region of Côte d’Ivoire and 302 farmers in eight villages in the western region of Ghana. Surveys, segmented focus groups and key informant interviews were conducted. The research adds to evidence from research on mobile money and cocoa farmers in Côte d’Ivoire by IFC and the MasterCard Foundation and USAID in Indonesia, it also builds on WCF’s 2011-2013 CocoaLink project, led by the Hershey Company and championed by the Government of Ghana.

The resulting analysis led us to develop a persona of a cocoa farmer who is likely to be an early adopter of mobile money – customers who could represent the frontier of more widespread adoption.

Awareness, use and interest

In Ghana and Côte d’Ivoire, 76% of the cocoa farmers in our survey own a mobile phone; in certain districts in each country mobile phone ownership is over 90%, according to estimates based on WCF’s 2014 research on the Cocoalink project. When it comes to mobile money, cocoa farmers have a high level of awareness (80% of those we surveyed). Fifty-two percent of farmers have a mobile money wallet, and 46% of farmers have had experience using mobile money services.

Although 13% have used mobile money to save and 5% have used mobile money to pay bills, it was mainly used for personal money transfer (51% receiving and 81% sending). Eighteen percent of survey respondents had received a mobile payment for cocoa sales in the most recent season; however, use was for the most part limited to money transfer for personal use.

Indeed, there is a continued reliance on cash in the cocoa value chain. In Côte d’Ivoire and Ghana, over 90% of cocoa sale transactions are still done in cash. Cocoa farmers are, however, integrating mobile money in other areas of their lives. Fifty percent of the farmers aware of mobile money have completed at least one transaction, but only 3% of farmers surveyed (and exclusively in the research sample in Ghana) indicated that any of these transactions were to receive a payment specifically for their cocoa crop.

Cocoa farmers express comfort with cash payments and are hesitant about the value of mobile money use for cocoa payments.

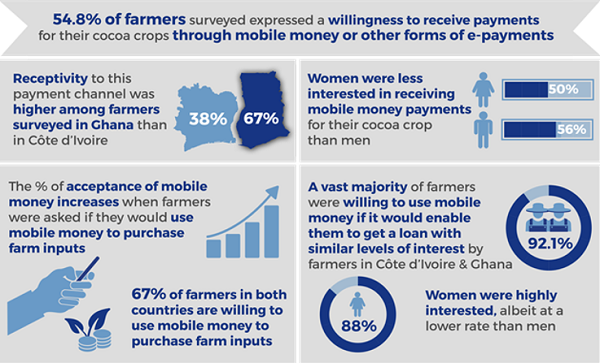

- Only 54.8% of Ghanaian farmers expressed a willingness to receive a mobile money payment for their crop; this percentage was below 50% in Côte d’Ivoire.

- Farmers’ top reported concerns with receiving mobile money payments centered around issues of mobile money agent access, liquidity, proximity and availability.

- Farmers also cited concerns with payment delays and technology literacy.

- In addition, the survey showed the greatest difficulties cited to collect cash from a mobile money transaction were network coverage (63%) and proximity to a cash-out point (12%). Yet concerns about agent proximity are hard to reconcile with the finding that 64% of the farmers in Côte d’Ivoire indicate there is a mobile money agent less than 1 kilometer away, and 43% of the farmers in Ghana reported they were within 1-5 kilometers of an agent.

The cocoa farmers’ level of interest in mobile money use increases, however, if digitizing payments could lead to services that would increase their ability to purchase farm inputs and access credit. Additional use cases also add relevance, such as the new requirement to pay school fees using mobile money in Côte d’Ivoire. These services would ride on the rails of m-wallet use, which can drive a digital financial identity that is elusive if the primary transaction mode is over the counter.

The future of mobile money with cocoa farmers

Our data analysis also led us to develop a persona of a cocoa farmer who is likely an early adopter of mobile money – “the professional farmer.” A professional farmer is one who has received formal education (primary or higher), has more than 10 years of professional cocoa farming experience, belongs to cooperatives or professional farming associations, reaps farm yields in excess of the median yield of 260 kilograms per hectare, and invests more than 5% of the cocoa sale proceeds back into their farms. The professional farmer had the two most highly correlated factors for those willing to receive cocoa payments through mobile money: (1) his or her awareness of mobile money, and (2) his or her segregation of money between farming activities and other household sources of income.

Among our sample of farmers, 28 fell into this category (27 in Ghana and 1 in Côte d’Ivoire). Strategies to integrate mobile money into the cocoa supply chain could start with targeting this group as part of an effort to develop “brand ambassadors” or peer leaders who would promote adoption by other farmers. This strategy has been used to influence mobile money use in other countries, such as Zimbabwe.

What’s next

With what we know now, how can we help to accelerate the broader awareness and adoption of mobile money products by cocoa farmers in Côte d’Ivoire and Ghana?

WCF is currently evaluating possible next steps, which could include a focus on the professional farmer as an early adopter and supporting work to:

- Map the payment chain for cocoa purchase and payment.

- Identify barriers and opportunities in the payment chain.

- Evaluate mobile money pilots with cocoa farmers as they progress, like the digital financial services offered by Advans to cocoa farmers in Côte d’Ivoire.

- Identify needs of cocoa farmers to promote uptake and regular use of digital financial services, both for their cocoa business as well as for general household financial management leading to better ability to invest in farming practices.

- Create partnerships with mobile network operators serving cocoa-producing areas to map agent network needs and liquidity.

Opportunity is great, given market conditions, to drive broader adoption of mobile money services that can improve farmers’ livelihoods.

Related Blogs

Building Rural Digital Ecosystems, One Small Payment at a Time

New research shows that digitizing everyday payments as person-to-person transfers can be a sustainable way for providers to reach customers in rural areas.

Building Rural Digital Ecosystems: A New Role for Agribusinesses?

Bringing digital finance to the rural poor will require financial services providers to work more creatively with agribusinesses that have extensive experience serving last-mile clients.

Add new comment