Fine Tuning Kaleido: A Key Step for Customer-Centricity

Early in 2014, Janalakshmi Financial Services, Jana Foundation, CGAP and Innovation Labs came together to develop a tool called Kaleido. Kaleido provides the foundation for building a customer-centric organization by providing a framework for understanding customers – their finances, businesses, attitudes, and life events.

Now that the framework has been established, Janalakshmi is refining it so that it can lead effective segmentation and mapping the right products to the right customers. As a first step, Janalakshmi piloted Kaleido with 1,118 ‘Accelerator’ customers to determine how the survey, with 1,000 data points, could be improved. The results of this initial questionnaire led to several findings and improvements in methodology. After this initial survey, the questionnaire was modified and retested with an additional set of 400 customers.

Lessons on data collection

The most basic realization after the initial survey pilot was that the survey questions were too complex and often resulted in responses that could not be analyzed. The working team also discovered that while information on family composition and household finances were fairly complete, data on attitudes, events and businesses were not adequate. In particular, the team learned five lessons:

1. Respondent fatigue: Due to the large number of data points captured, response fatigue was inevitable for both respondents as well as administrators. This resulted in blanket responses given to get the “interviewer off their back” or lack of responses resulting in several blank fields. The second round survey of 400 customers proved to be far more effective in terms of complete data capture, and allowed verification where existing fields had been filled in round one.

2. Quality control: A critical differential between the first and second rounds of data capture was the strict quality control in round two. This was done through strict monitoring by a Janalakshmi staff member who was familiar with customer profiles and would examine the Kaleido data at the end of each day to ensure data completeness and error free capture.

3. Events: Across both sets of data gathering exercises, information about life events, such as births, deaths, major illnesses or weddings, and their impact on people’s financial lives has been hard to capture. These details are fairly complex, but extremely important. For the team at Janalakshmi and CGAP, the key learning from this exercise is that it is hard to uncover this data by asking direct questions. As Kaleido is refined as a tool for data capture, this is an area that will require significant innovation.

4. Attitudes: The questionnaire attempted to capture responses by providing statements and getting customer reactions to these. However, the manner in which the statements were framed cued some of the responses. In the next phase, there is a plan to map psychometric profiles to capture information on this dimension.

5. Business: Business related queries regarding stock shelf life or initial capital investment were difficult for customers to recall. This is probably a specific characteristic of small businesses, where customers do not maintain a clear differentiation between household and business finances, making it difficult to account for some of these aspects. The team at Janalakshmi has observed a set of customers who begin to separate their accounting of household and business finances as the businesses mature. In the next phase of Kaleido, there will be a focus on this set of customers, allowing for a richer understanding of business finances.

Lessons from customer segmentation

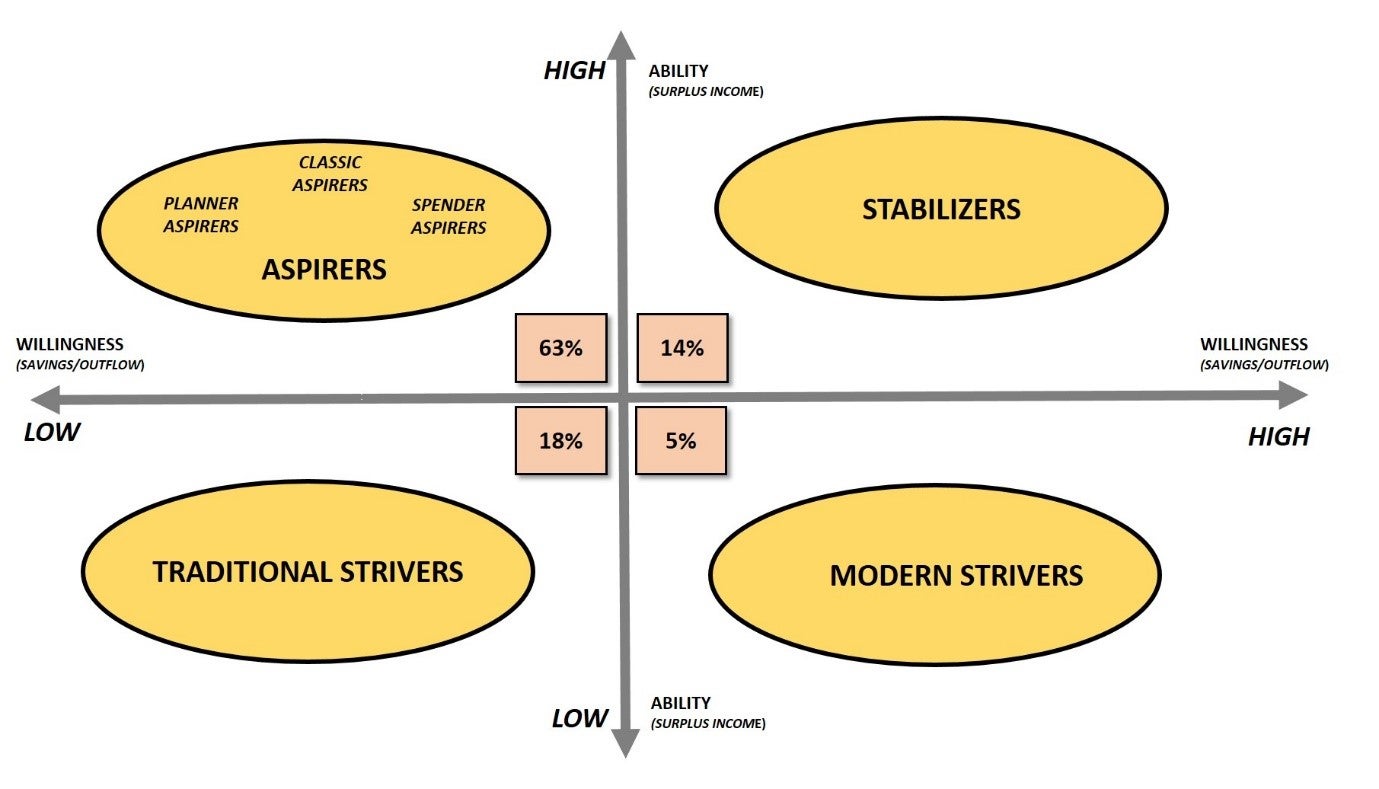

Once the survey was modified and data was determined “usable”, the team looked at whether there were natural clusters or segments of customers that emerged. Three areas of divergence became clear after analyzing the data: customers’ income levels (either high surplus or low surplus), customers’ willingness to save, and customers’ ability to save. Four specific segments emerged from this research:

- Stabilizers are households who have a high surplus income, high ability to save, and high willingness to save.

- Aspirers are households with a high surplus income, high ability to save, but low willingness to save – they often choose to spend instead. This segment was large, so sub-segments were created by tracking households that depended on A) a single income earner, called planner aspirers B) multiple income earners, called classic aspirers and C) all family members work so there are no dependents, called spender aspirers, to contribute to household income.

- Traditional Strivers do not have much surplus income, so they have low ability to save, but choose to save what they can in the form of traditional products like gold or land.

- Modern Strivers do not have much surplus income, have a high willingness to save, and do so in the form of formal savings products.

Conclusions and next steps

The new segments were presented to the business teams, including product development, sales, strategy, Information Technology and analytics, and have been found to be insightful in the following ways:

- Mapping customer segments to existing SEC segments to check correlation for credit appraisal and credit risk

- Identifying segments for recommending goal based savings products

- Map customer segments to the Financial Advisory Services (FAS) process

The next step in the process is to create a new version of Kaleido that is easier to implement with a shorter questionnaire – Kaleido Lite. Additionally, Janalakshmi is working to change some of the behaviours of certain customer segments to be sure they are able to separate business and household finances. Janalakshmi plans to use Kaleido Lite and its partner tool – the Arthika Nakshe wealth map – to map approximately 70,000 customers. This will yield rich data for the organization and for customers, this process will help them start thinking of their financial lives in the future.

Resources

Also in this Series

5 Ways to Improve Customer Experience for the Poor

CGAP offers five insights on improving customer experience for the poor, in ways that are game-changing, yet profitable.

Can a Good Customer Experience for the Poor Benefit Business?

Is it important that financial service providers (FSPs) provide a good customer experience when serving poor, underbanked customers? Evidence says "yes," but this is often overlooked by FSPs.

Add new comment