What Keeps People from Paying with Their Phones?

Ever since M-Pesa caught the world’s attention in 2007, East Africa has been ground central for companies offering services that can be paid for using mobile money to the bottom of the pyramid. Pay-as-you-go (PAYGo) solar providers have reached upwards of 800,000 households in Kenya, Tanzania, and Uganda — markets where customers are able to repay the loans for their solar devices through mobile money. But what happens when PAYGo products are introduced into markets where few people are used to making payments on feature phones (in other words, almost everywhere else)? CGAP explored this question by partnering with PEG Africa, a PAYGo solar company operating in West Africa, and Tigo Ghana, the country’s second largest mobile network operator.

Mobile money in Ghana

Mobile money in Ghana has taken off only in the past few years. Until 2015, it was technically illegal for a nonbank to own an e-money platform, which left mobile money in the hands of banks that were uninterested in, or ill-suited for, the costly task of building up national agent networks. Once mobile network operators were permitted to offer mobile money services, they applied a strategy to reach scale quickly by deploying agents and paid minimal attention to educating customers about how to use their services. This helped create an over-the-counter market where agents effectively operate customer’s mobile wallets for them. And although over-the-counter service may lead to or complement mobile wallet use, it has notable drawbacks for some advanced services.

Mobile money payments, the foundation of PEG’s business model, are one of these services. As in the M-Kopa Kenyan model, PEG finances the sale of a solar home system, allowing users to pay for the system over a 12-month period. Loan repayments are tied to use, so if a user runs out of prepaid days, the unit shuts off until he or she makes another payment. Ideally, customers pay early and often, their devices are never shut off for failure to pay, and they finish repaying on or ahead of schedule. Mobile payments are the key to making this happen, as they are the quickest and cheapest mode of payment.

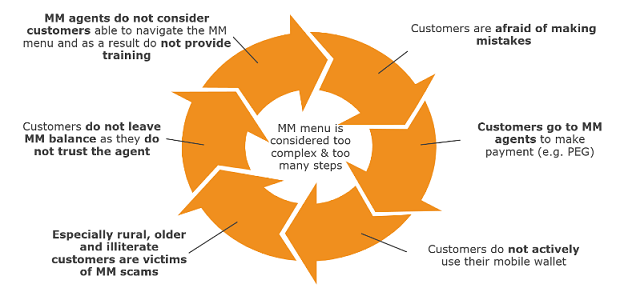

Yet in 2016, only 24 percent of PEG’s payments arrived via customers’ own mobile wallets. About 76 percent of payments were made by customers through someone else’s mobile wallet — typically, over the counter with mobile money agents or PEG field staff. Relying on someone else’s mobile wallet creates delays, higher costs and inconvenience for the customer. This results in less light for customers, longer paybacks for PEG, and decreased mobile wallet use.

Insights for increasing mobile money payments

Together with PEG, CGAP set out to come up with generalizable strategies to increase mobile payments among customers. The project began with a three-month research period, followed by a five-month pilot phase. Three main learnings came out of the initial research:

- PEG’s customer base is used to passive payment methods. The Ghanaian payments sector has been designed for user convenience, and services providers are often actively involved in the payments process. This is not only the case for over-the-counter mobile money, but also for informal payments schemes. A well-documented Ghanaian example is the susu, a savings scheme whereby a collector visits customers everyday to collect deposits. Another example is the informal “lottery,” in which participants buy lotto tickets for cash when a seller visits them. A final example is utilities that send payments collectors to users’ homes. When passive payments are common, requiring customers to be actively engaged in the payments process disrupts the status quo.

- PEG customers are skeptical of using mobile money for anything beyond person-to-person transfers. One of the inherent disadvantages of an over-the-counter mobile money market is that, by relying on mobile money agents and other providers to make payments, customers never become familiar with mobile money technology. This, in turn, creates opportunity for fraud. In fact, 80 percent of customers interviewed for this research reported having to pay additional charges on top of operator fees when paying via a mobile money agent, making them mistrustful and averse to using mobile money. Most customers, whether paying on their own or with the help of an agent, said that they call PEG every time they make a payment to confirm it has been received. This creates unnecessary call volume, and breaking this cycle is critical for PEG to create a sustainable business model.

- Mobile money agents are not a reliable payments channel. Relying on mobile money agents presents some issues. First, agents do not always have sufficient e-money to exchange for cash, which forces customers to search for agents with liquidity. Second, while agents earn a higher commission on mobile money payments than they do for cash-in/cash-out transactions, mobile payments are more time-consuming because they often present complications that need to be resolved by the agent. For instance, rejected payments sent from an agent’s mobile money account are returned to the agent (not the customer), so customers hold agents responsible for resolving failed payments. Because of these complications, some agents choose not to let customers make payments over the counter. One agent even began to show customers how to make payments from their own phones after cash-in, forfeiting the commission but saving time.

What's next?

While PEG initially considered over-the-counter payment through agents a viable payments channel for customers unable to navigate the phone menu, the field evidence shows that agents are costly, sporadically available, and often charge added fees. This research provides the rationale for piloting alternative payments methods to reduce the barriers for self-payment.

In a follow-up blog post, CGAP explores the innovative methods used by PEG to make mobile payments more acceptable (and more commonly used) by rural customers in Ghana. The results are exciting and show that even in countries where mobile money is unfamiliar (70 percent of PEG’s customers had never used mobile money prior to PEG), the PAYGo business model can still grow sustainably.

Related Blogs

Building Rural Digital Ecosystems, One Small Payment at a Time

New research shows that digitizing everyday payments as person-to-person transfers can be a sustainable way for providers to reach customers in rural areas.

How Ghana Became One of Africa’s Top Mobile Money Markets

Mobile money account ownership tripled in Ghana from 2014 to 2017, making the country one of the fastest growing mobile money markets in Africa. How? Smart regulations played a key role.

Comments

That is an interesting study

That is an interesting study and one it would be good to use as a basis for further work. Perhaps the key to confident usage of mobile payments is encouraging the merchants - rather than agents - to be the cashing out point for the phone owner. The interesting area to address in this sector is whether the business model allows for very low or zero interchange fees for the merchant; it is clearly attractive for the merchant to encourage frequent shoppers to use their funds for staple needs - and only cash out the balance.

While credit and bank debit cards continue to charge relatively high fees to merchants - in the 2% to 5% range - one area where these may be under pressure is from crypto currencies where the fee format can be down to zero for both the merchant and for the two main sources of funding, i.e. from family remittances and from payroll distribution.

This policy can work with a lottery or incentive structure, where the merchant is an equal partner with the customer in any reward format. There are a variety of ways in which any such award settlement can be secured to ensure the customer is genuine, understands what he or she is getting - and in the case of a significant amount, gets help in how to invest or allocate their good fortune.

The fundamental value of mobile payments is far too great to risk it being destroyed by agents cheating the phone owner, which is clearly the critical issue here. While we work to get remittance fees down to below the 3% SDG target, the settlement process needs a lot of attention.

Each country will have its own particular nuances, and therefore has to be addressed specifically, but moving across to domestic clearing of utility bills from a central clearing, with a central investment point for customers to purchase insurance and apply for loans - and a merchant/customer relationship where neither is paying fees for all other shopping is a good starting point.

Thank you for your

Thank you for your contribution and thank you for sharing ideas Christopher. I agree that merchants will be key for unlocking mobile payments. Cash keeps on winning in this market because of its convenience, reliability and perceived low costs. Not to speak of course for the lack of network coverage, lack of reliable access to energy and lack of trust in mobile payments. PAYGo solar provides an incentive for people to start paying with mobile money because of the value proposition it holds for their customers; access to reliable energy outweighs the investment to learning the technology and taking time to load money. However, the value proposition for high frequent payments, such as payments at mom&pop stalls, still has a large gap to overcome and depends on their context as you already outlined.

Lowering the barriers to making payments increases the likelihood of the customer to taking up mobile payments from their own phone, which is the approach we took for this project to incentivize payments. Read in our next blog how we did this and its impact: http://www.cgap.org/blog/can-user-friendly-payment-methods-improve-repa…

ln Pakistan, like many other

ln Pakistan, like many other developing countries, the challenge remains to strike a serious dent on the cash economy that is keeping the majority excluded from formal financial services. The prevalence of cash economy is mainly due to the majority of population having developed oral techniques of their own to deal with financial matters. In other words, this majority has learnt to do its financial arithmetic with the help of cash notes. If you take cash out of transactions, they are unable to understand them.

The cashless transactions present a calculation and trust challenge for the majority of population that is why they want to keep away from them, otherwise they have nothing much against them. The branchless banking agents are actually filling the gap that exists between the financial services provides and their consumers. In other words, people are able to use their oral skills with agent and cash.

While designing mobile banking applications, we need to recognise oral skills of the majority. Interested readers may refer to the work of My Oral Village at myoralvillage.com. Two recent blogs by Brett Matthews, Executive Director at My Oral Village, are very useful. These are available on LinkedIn as "Designing for Oral Financial Inclusion (1)" and "Designing for Oral Financial Inclusion (2)".

Dear Aqeel,

Dear Aqeel,

Thank you for your comments. On the cash-in side, I think there is no doubt that what you say is correct: agents have an invaluable role to play, essentially acting as the customer 'interface' for complex payment procedures. We ran into issues with agents making bill payments, but that more reflects their incentive structure and the trajectory of the Ghanaian market.

When it came time to design actual payment strategies, My Oral Village was one of the chief inspirations for the Pay-Over-Phone product, which allows people to make payments through a trusted (and human) relationship. As DFS-enabled businesses look to scale rapidly, however, it will be interesting to see whether developing these relationships becomes a bottleneck. For instance, we explored the idea of incorporating Interactive Voice Response (IVR) into the product, which could allow users to make a payment by interacting more comfortably (and orally) with a service that could initiate 'pull' payments.

Thank you for your sharing

Thank you for your sharing your insights on My Oral Village Aqeel. I completely agree with the approach to let the technology work for people, instead of against them. In my opinion, digital finance has the potential to make payments event easier than cash if carefully designed with the end-user in mind. We are only at the beginning of this movement and there is still a lot of potential innovation to take place.

For this project we did exactly that, by piloting payment methods that lower barriers for customers to make digital payments. Read in our next blog how we did this and their impact: http://www.cgap.org/blog/can-user-friendly-payment-methods-improve-repa…

Add new comment