Advocates for pay-as-you-go (PAYGo) solar financing have often touted the potential of electrification to improve school performance, pointing to light as critical to allowing children to study at night. But one provider in Uganda is proving that an often-overlooked benefit of PAYGo – financial inclusion – can also affect education outcomes by keeping kids in the classroom.

That’s the takeaway from a new impact evaluation study of Engie Energy Access’ (formerly Fenix Intl) ReadyPay school fee loans in Uganda, a product designed in collaboration with CGAP under the Harnessing Innovation for Financial Inclusion (HiFi) program. The randomized control trial implemented by researchers from UC Berkeley and Washington University, with the support of the IFC and CGAP, found that these small cash loans offered to solar home system borrowers impacted the ability of poor, rural households to send their children to school.

Low-income households have few options to smooth consumption and pay for education

The households that participated in the study belong to some of the most financially excluded and difficult-to-serve customer segments. Over 70 percent own or operate a farm, and about 50 percent own a microenterprise – occupations that are associated with unpredictable and irregular cashflows. Additionally, 30 percent live below the middle-income poverty line of $3.10 a day. Not surprisingly, these households have few formal financing options. While most had borrowed in the past 12 months, only 14 percent had a bank loan, and just 7 percent had a loan from a microfinance institution.

Without access to formal credit, many households reported difficulty paying school fees before taking a ReadyPay loan. “'I used to get the money from my business. This was greatly affecting the business,” explained one of the participants, a small business owner named James.

At the same time, households that were interested in the school loan reported placing a high value on education. Almost all agreed that children should not be kept home from schools and that keeping children in school would be critical to their future employment prospects. But for these households, school attendance often strains household finances. In about 1 in 10 households with at least one child between the ages of 5 and 20, a child was not enrolled in school because the family could not afford to pay school fees, books or uniforms at baseline. These households reported that school-related expenditures amounted to 7 percent of household income per child. With an average of three children per household, these expenses quickly add up.

Study finds loans have a clear impact on school attendance, spending on education

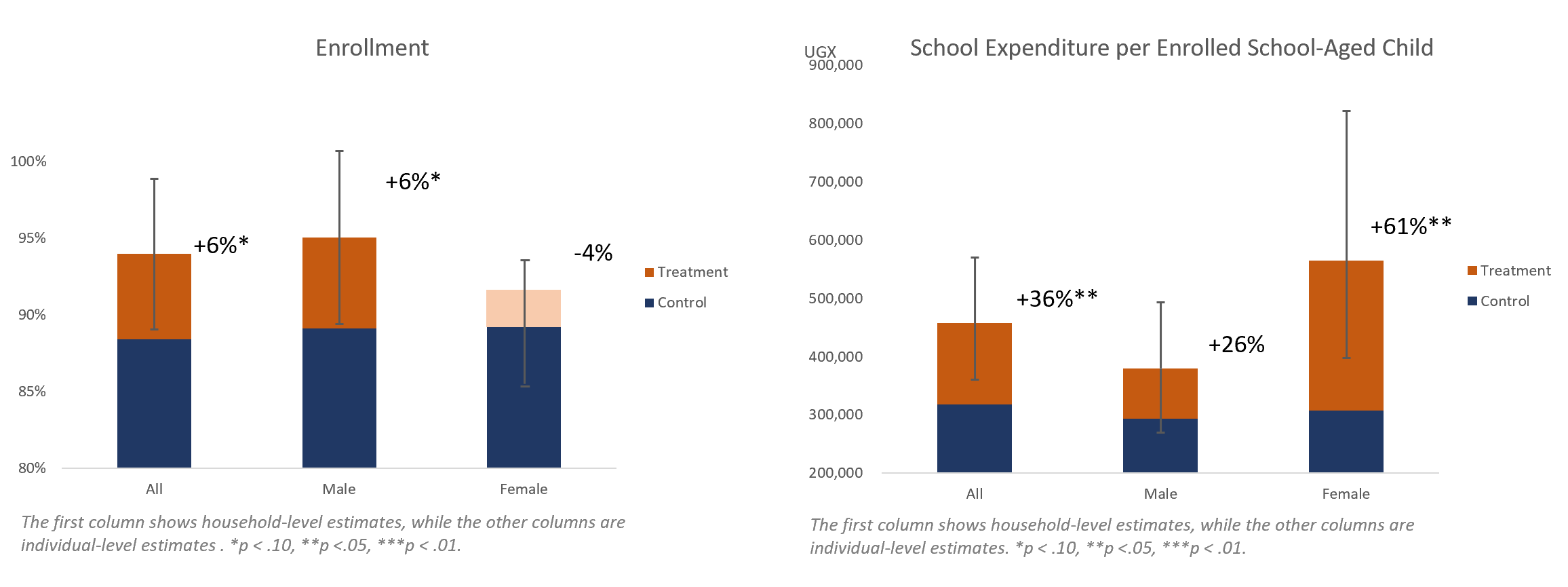

Six months after being offered the ReadyPay loan, children in households that received a school fee loan were far more likely to enroll in school compared to children in the comparison group. In fact, the loans led to a 50 percent reduction the share of children out of school. Households who received a school fee loan increased their education-related expenditures by 36 percent, including spending on school fees, supplies (uniforms, pens, pencils, notebooks, etc.), transport and school meals. Whereas the loans had a larger impact on boys’ attendance, the increase in expenditures was more concentrated among girls.

While the exact mechanisms for these differences are not entirely clear, CGAP would welcome more research on this issue.

Gladys, whose child had been sent home from school before when she wasn’t able to pay school fees, expressed gratitude for her ReadyPay loan: “My child is able to go to the school on-time and doesn't miss any days.”

Despite initial concerns, loans appear to not over-indebt borrowers

The study sheds light on two important considerations related to the impact of taking out debt for school expenses. CGAP has previously raised the issue of over-indebtedness for households taking out PAYGo loans, with qualitative research suggesting that PAYGo customers sometimes struggle to meet their repayment obligations. However, the study didn’t find significant changes in household finances, such as selling assets or borrowing from other sources to repay school fee loans.

Second, CGAP and Energy Access were initially concerned that taking out a school fee loan could make it harder for customers to repay their solar loans. Since PAYGo-financed solar home systems are locked when customers fail to repay — referred in the study as “digitally repossessed” — this could lead to their lights being shut-off. To put this into context, Engie Energy Access customers typically use their solar system 6 to 7 days per week and approximately 10 hours per day. While the study doesn’t offer a definitive answer on whether school fee loans had this effect, borrowers’ systems were locked only 16 out of 100 days, on average, suggesting that school fee loans did not significantly impact access to energy.

Importantly, almost all households reported satisfaction with their borrowing experience. Indeed, nearly all customers told researchers that they would take another loan in the future and would recommend the loans to others.

“I don't regret getting the loan. The whole process was very easy, and I received the money in a short period of time,'' one borrower responded, when asked to explain why she would recommend the product to a friend.

Overall, the study’s results point to an opportunity for PAYGo — and asset financing more broadly — to serve as entry point to formal financial inclusion and unlock access to financing for critical needs like education. It also points the way for providers to develop sustainable lending models that can drive real impact for poor households, a topic that we will revisit in a second blog in the coming weeks.

Also in this Series

Flipping the Switch: How Locking Assets Unlocks Credit for the Poor

A new study out of Uganda offers strong evidence that lock-out technology can enable providers to sustainably lend to low-income customers, who may need credit for school fees and other critical expenses.

How Bangladesh Digitized Education Aid for 10 Million Families

In just months, Bangladesh digitized financial aid payments for education to millions of families. What can other countries learn from this rapid transition to digital payments?

Add new comment