Pakistan Enigma: Why Is Financial Inclusion Happening So Slowly?

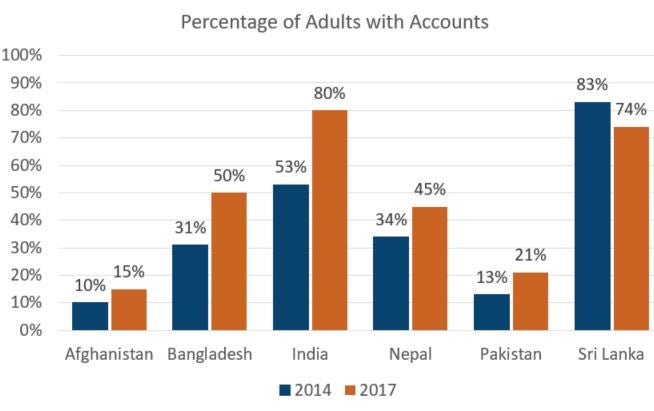

On the eve of the 2017 Findex, many observers expected to see rapid progress in Pakistan. The country’s longstanding commitment to financial inclusion, including the adoption of a national financial inclusion strategy in 2015, led some to predict that the percentage of the adult population with accounts had quadrupled over the past three years, from 13 percent to 40-50 percent. Yet the 2017 Global Findex revealed only modest growth since 2014, with 21 percent of adults having accounts. Why?

Pakistan’s head start on financial inclusion

It is easy to see why expectations were so high. Pakistan adopted financial inclusion as a national priority well before many other countries did. Support of the microfinance sector dates to the 1990s, and in 2001 the government began to allow the creation of microfinance banks. In 2008, Pakistan became one of the first countries to adopt branchless banking regulations, which paved the way for digital financial services. This support intensified in 2015, when the national financial inclusion strategy was approved.

Thanks largely to these policies and regulations, Pakistan today has a strong and growing microfinance sector and more than 10 banks that offer digital financial services, the largest of these owned by mobile telephone companies. This enabling policy environment has encouraged private sector investment in microfinance institutions and digital financial services providers, which has helped to fuel the growth of the financial sector.

Beyond putting in place an enabling policy environment, Pakistan was also early to digitize government payments. In 2010, its Benazir Income Support Programme began to digitize safety net support to 6 million poor women, and many other government programs have gone digital since then. In 2014, Pakistan became a member of the United Nations’ Better Than Cash Alliance, which encourages governments around the world to use digital payments.

Pakistan also has better market infrastructure to support financial inclusion than many countries. This includes the national ID authority’s (NADRA’s) biometric ID database, which covers most adults, and a privately owned switching and clearing company, 1Link, which includes almost all banks.

Progress is slower than expected

Despite these advantages, the percentage of adults with accounts rose just 8 percentage points from 2014 to 2017, bringing the total to 21 percent. InterMedia's 2018 Financial Inclusion Insights Survey corroborates the Findex numbers.

As “Measuring Women’s Financial Inclusion: The 2017 Findex Story” points out, Pakistan’s gender gap has actually widened considerably since 2014. In 2014, 21 percent of men had accounts, and this number increased 13 percentage points to 34 percent in 2017. By contrast, the percentage of women with accounts increased just 2 percentage points from 5 to 7 percent. This means that men are now roughly five times more likely than women to have an account.

What’s slowing Pakistan down?

Some observers have pointed to the Pakistani public’s mistrust of banks and other formal institutions as a reason for Pakistan’s slower-than-expected progress. The Gallup World Poll 2017 offers some support for this idea, showing that more than a third of adults in Pakistan do not trust financial institutions. If it is true that trust is low, improving financial inclusion in the short term may be more difficult than previously thought.

While building trust is a long-term challenge, improving financial services providers’ capacity and ambition to reach large scale, especially with mobile wallet account ownership, can be addressed in the shorter term. Recent CGAP research reinforces the indispensable role that executive commitment and investment play in scaling up financial inclusion businesses. While we can only speculate as to why providers have not invested enough in Pakistan, the numbers reveal that a decade of investment has resulted in only 37 million mobile wallet accounts in a country of 208 million people, just 22 percent of which are registered to women.

The State Bank of Pakistan (SBP) reports that 52 percent of these accounts are active, while businesses themselves report a much smaller percentage of active wallets, possibly less than 20 percent. The dominant use cases remain limited to mobile top-up (45 percent of all transactions) and cash-in and cash-out (26 percent), with far fewer person-to-person transfers (17 percent) and bill payments (less than 10 percent).

Moving routine cash transactions into accounts could help reduce the share of unbanked adults in Pakistan. Digitizing bulk payments is one opportunity. Findex reports that 9 million unbanked adults receive wages in cash only. Among adults who rely on agricultural payments, 7 million are unbanked and receive payments in cash only. At the same time, nearly two-thirds of the adults receiving such payments in cash own a mobile phone.

What's next?

- Will Ant Financial be a game-changer? Ant Financial’s $184.5 million purchase of a 45 percent stake in Telenor Microfinance Bank, which houses and manages EasyPaisa, could be a game-changer. Ant Financial’s involvement could quickly turn EasyPaisa into a runaway market leader, spurring other businesses to become more ambitious about increasing mobile wallet uptake and use. The deal also establishes an investment benchmark in the market that could encourage additional investment into other FinTech businesses. At the same time, a rapidly expanding EasyPaisa business could prompt SBP to be more open and innovative as it tries to keep pace with new business ideas and practices.

- Will regulators be even more innovative? For the past two decades, SBP has led Pakistan’s commitment to financial inclusion. At least until 2011, the market responded positively to opportunities created by SBP. Looking back, however, it appears that SBP could have pushed innovation even earlier and further. For example, SBP had the authority to issue enabling regulations for nonbanks as early as 2007 but came around to it only in October 2018. Allowing the licensing of nonbank e-money issuers earlier could have spurred innovation and growth. And the lack of a comprehensive national payments systems strategy has meant uncertainty in the market and lost opportunities. Implementing enabling regulations faster could spur more rapid progress.

- Can shared financial infrastructure make a difference? Market-level financial infrastructure includes the institutions and systems that allow retail financial services to operate, such as payment schemes and ID systems. When connected, these components can improve transparency, promote competition, lower provider costs and make financial services more affordable and accessible for the poor. Open banking initiatives in other countries demonstrate the potential of such connected market systems. Pakistan has the necessary components, but they are not connected in optimal ways or treated as utilities. As a result, digital financial services remain largely siloed. Businesses owned by mobile telephone companies have exclusive connections to their mobile telephone company, leaving commercial banks and FinTechs excluded from important infrastructure. Initiatives are underway to improve the situation, but these are not expected to be operational within the next two years. Even then, it is unclear how all the infrastructure elements will be connected.

Pakistan faces many financial inclusion challenges, but other countries have experienced strong growth in financial inclusion through sound approaches that are well documented. Pakistan need not reinvent the wheel.

Also in this Series

India Moves Toward Universal Financial Inclusion

The 2017 Findex shows India has made significant financial inclusion progress in the past four years, but use remains a challenge.

Financial Inclusion: Is the Glass Half Empty or Half Full? (Pt 2)

The number of people with financial accounts has grown rapidly, but account dormancy remains a problem, especially in Sub-Saharan Africa and India.

Comments

For market penetration of…

For market penetration of DFS , there is an imperative need to increase the stake of mobile companies to impart digital numeracy and financial literacy to the poor clients in informal sector particularity adults and women.

Add new comment