Pakistan: Is Mobile Money a Viable Alternative to Banking?

In a world where 2 billion adults lack access to formal financial services, Pakistan is no exception. The 2014 Financial Inclusion Insights (FII) survey estimates that 93% of Pakistani adults are financially excluded as only 7% of the respondents reported to having a bank account, while registered accounts with other financial institutions were negligibly low.

A more promising statistic is that of mobile phone ownership, as the FII survey finds that 54% of Pakistani adults own a mobile phone. This high proliferation of mobile phones is considered by many to be an opportunity for the financially excluded to attain financial inclusion through Mobile banking.

The hope is not at all misplaced if one only considers the proliferation of mobile money in Pakistan during the last few years. According to the latest statistics from the State Bank of Pakistan (SBP), Pakistan’s mobile industry in the quarter January-March 2015 has a come a long way from what it used to be during July-September of 2011. For starters, at the end of September 2011 the total number of active agents stood at 15,829, a number which has now grown to 183,117 at end of March 2015. Similarly, the number of active Branchless Banking accounts (mobile money accounts) have seen a 5 fold increase. Transaction volumes have increased seven fold in the same time period.

The biggest contributor to this growth is the phenomenon of over-the-counter (OTC) transactions. By leveraging the proximity and familiarity of local grocery stores and mobile money shops, OTC transactions have made bill payment and person-to-person transfers much more convenient than alternatives, such as banks or hawala dealers. This convenience is getting recognized by the market as proven by the tremendous growth in these transactions.

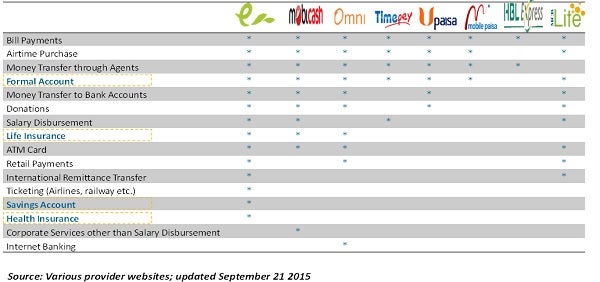

However, there is more to financial inclusion than just convenience. When it comes to offering a variety of financial services, can mobile money companies be truly considered as alternatives to regular banks in Pakistan? Do mobile money companies offer loans to those facing a financial crunch? Do they incentivize savings through interest bearing saving accounts? Because unless products such as loans, insurance, and interest on savings are offered by mobile money companies, they can’t really be considered as a lifeline for the financially excluded.

A look at the services offered by mobile money companies in Pakistan shows that none of the companies offer loans. Similarly, only one company, market leader Telenor’s Easypaisa, offers an interest-bearing savings account. Only three companies - Telenor’s Easypaisa, Mobilink’s Mobicash, and UBL Omni - offer life insurance products while Telenor’s Easypaisa also offers health insurance.

Mobile money providers seem focused on providing bill pay and remittance services (transfers through agents or transfers to bank accounts). However, according to the Global Findex survey 2014 for Pakistan, the demand for saving and borrowing products is actually higher than that for sending and receiving remittances. Thirty-two percent of Findex respondents reported having saved money during the last year; in comparison only 25% reported receiving remittances in the last year. If mobile money companies could provide ways for people to save and borrow digitally, they could fill a gap in the market and serve a larger group of people than just those interested in remittances.

Pakistan’s National Financial Inclusion Strategy 2015 states its vision as follows; “individuals and firms can access and use a range of quality payments, savings, credit and insurance services which meet their needs with dignity and fairness.” Mobile money has the potential to help achieve this vision and provide financial inclusion to those who need it. But for that to happen, it first has to provide the services that are needed for providing financial security. Unless such services are offered, the rise in the number of mobile money accounts will not translate to greater financial security for the financially excluded of Pakistan.

For more information, please refer to "Using Mobile Money to Promote Financial Inclusion in Pakistan, by Karandaaz Pakistan."

Also in this Series

Making Mobile Money Accessible in Pakistan

Mobile wallets could have a revolutionary impact on financial inclusion in Pakistan. However, success of this channel hinges on matching the abilities of the end users with appropriately designed products.

The Promise of Mobile Money in Pakistan

Mobile money - through over the counter services and mobile wallets - is helping to drive financial inclusion in Pakistan.

Comments

Pakistan's dilemmas are

Pakistan's dilemmas are similar to other neighbouring countries where in the absence of legacy landline telephony, mobile has grown in leaps and bounds and has become a low cost and fast medium for remittance traffic. Though it fulfills an important need but is it the end for the financial inclusion is a moot question. A major reliance on mobile and not developing bank branches and their agent infrastructure can only be labelled a practice of lazy banking. Banking regulators are in a way abdicating their responsibility by not insisting on innovations in branch banking structures so as to make these low cost and have a wider geographic spread. Heavily regulated banks are the only institutions of trust which need to be offered to poor public on long term basis. The onus on government-owned banks is still more to offer doses of required productive credit so as to support informal entrepreneurs, in the absence of jobs, amongst illiterate and poor masses. South Asian countries bound by one culture can benefit merely by looking across borders and further built up on where one country has reached. Neighbours can learn a lot from the successful Pakistani mobile money experience, while it can also benefit vice versa. Cause of removing poverty from Pakistan and indeed entire South Asia through financial inclusion being the goal and mobile money needs to be considered only one successful step in the long and arduous journey.

Add new comment