Growing Up, Growing Informal: Gender Differences in Financial Services

Gender-disaggregated data is the first step toward creating gender-transformative solutions in financial inclusion. Despite the growing number of financial inclusion datasets in low-income countries, detailed analyses of the often different ways women and men access, use and benefit from financial services — and data-gathering approaches designed to enable such analyses — continue to be scarce. Analyses that trace differences in women’s and men’s financial behaviors over long periods of time are even rarer.

This paucity of information can be attributed to a combination of factors, ranging from a perceived lack of value to concerns that gender-disaggregated data collection is expensive. While well-designed, exhaustive data collection exercises can indeed be resource intensive, there may be ways to mine existing datasets to provide initial guidance on research gaps and catalyze research.

Building on an earlier analysis of Findex data, CGAP recently worked with Finmark Trust to conduct a gender-disaggregated analysis of existing Finscope/FinAccess data. Our goal was to find out what, if any, gendered patterns these large-scale datasets could reveal about how people use financial services over their lifetimes. We focused our analysis on Kenya and South Africa due to the size of the available datasets and the diversity in their financial systems. Here is what we found.

Women opt disproportionately for informal financial services, regardless of income or education

Our analysis provides quantitative confirmation that gender influences people’s preferences for formal vs. informal financial services. In both Kenya and South Africa, the data suggest that women’s preference for informal services is driven by a “gender residual,” regardless of income and education. In other words, even when education and income are controlled for, women prefer informal services.

A number of qualitative studies (such as those by Zollman and Sanford (2016), Johnson (2016) and Oware (2020)) help explain what could be driving this gender residual. These factors include the gendered division of opportunities; priorities and responsibilities across life stages in different contexts; the role informal financial services often play in women’s social networks; and the fact that informal products are well suited to the type of low-value, high-frequency transactions that typify women’s transaction patterns.

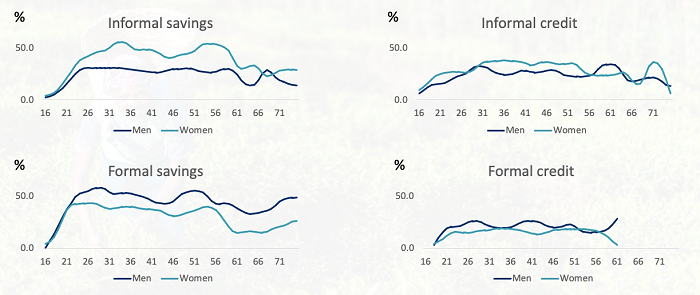

Women’s relative informality becomes pronounced only in their early 20s

Adoption of formal accounts rises quickly for both girls and boys during their late teen years but then diverges sharply. In Kenya, there is an inflection point in women’s adoption of formal credit and savings services when they reach their early 20s. Particularly for formal savings, adoption rises fast in the late teen years, with virtually no gender gap. However, adoption rates begin to flatten for women in their early 20s, while men continue to adopt formal financial services. For informal financial services, this trend is reversed.

Age curves for access to formal and informal savings and credit in Kenya

We observed similar dynamics in South Africa. Across both countries, the women who access formal financial services seem to do so fairly early in life. Between their early 20s and 30s, women begin opting for informal services at a higher rate than men, while the opposite is true for formal services.

Data analysis reveals both straightforward and complex drivers of gendered behavior

What happens in the lives of young women and men in these two countries that seemingly determines their lifelong adoption of formal vs. informal services? Existing financial inclusion data hint at what may be driving these patterns. To mine the data for these insights, we conducted regression analyses covering dozens of variables included in the two datasets. We wanted to see if we could uncover what factors were associated with financial inclusion patterns in men and women as they age.

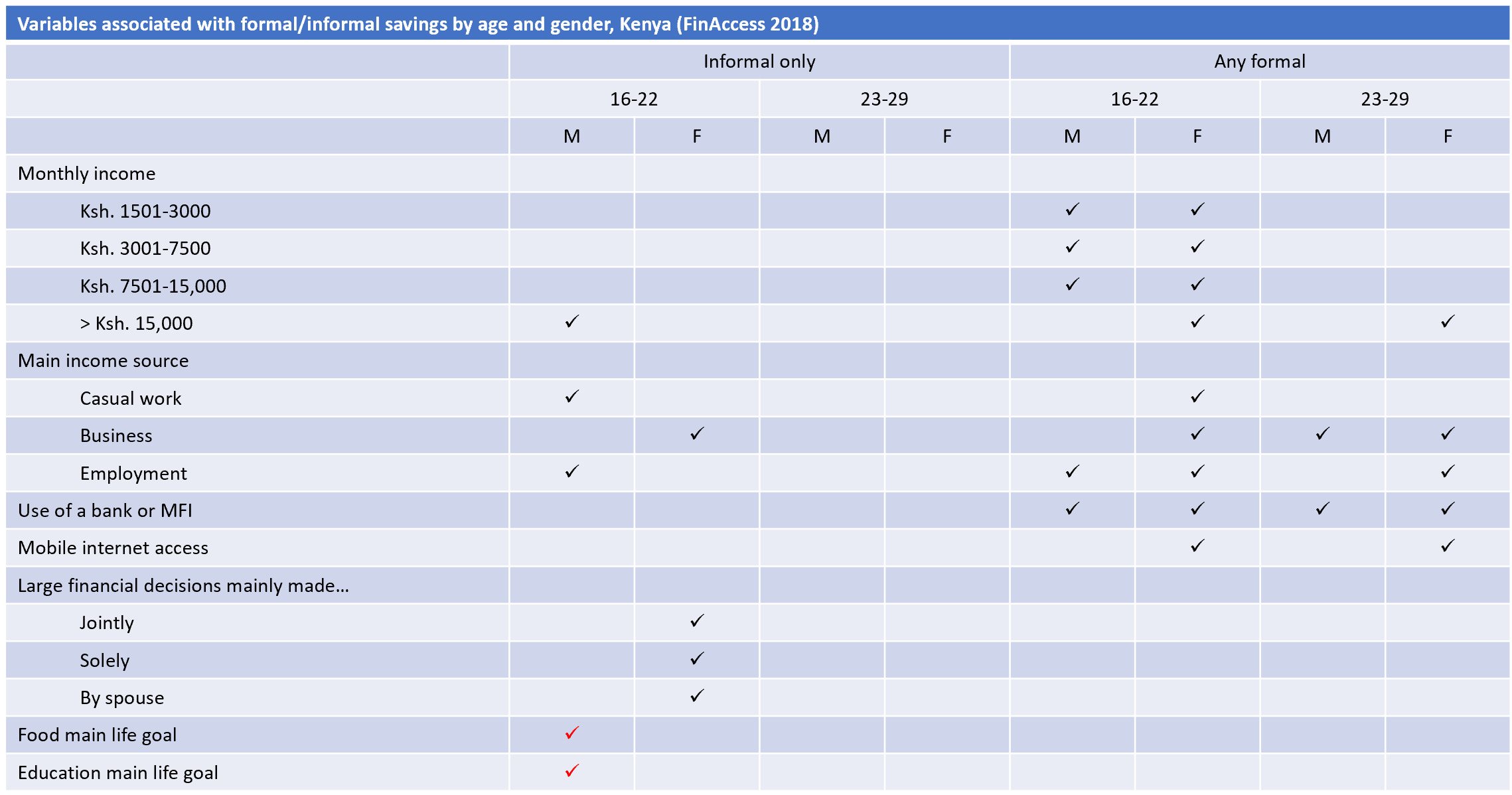

In Kenya, we looked at differences in behavior among women and men just before and after the inflection point seen in the curves above (i.e., 16 to 22 and 23 to 29). We found several “usual suspect” factors associated with women’s and men’s adoption of formal savings. Higher income levels, main income from business or employment, and use of a bank or microfinance institution were all associated with formal savings women and/or men.

However, more complex associations also emerged. For example, income from casual work was associated with formal savings among women ages 16 to 22. Among men in the same age group, it was associated with informal savings. Several different patterns of household financial decision-making appeared to push women ages 16 to 22 to save informally, while certain goals seemed to discourage men 16-22 from saving informally. There may also be other factors contributing to the gender residual that are not captured by the variables in this dataset.

Variables associated with saving in Kenya

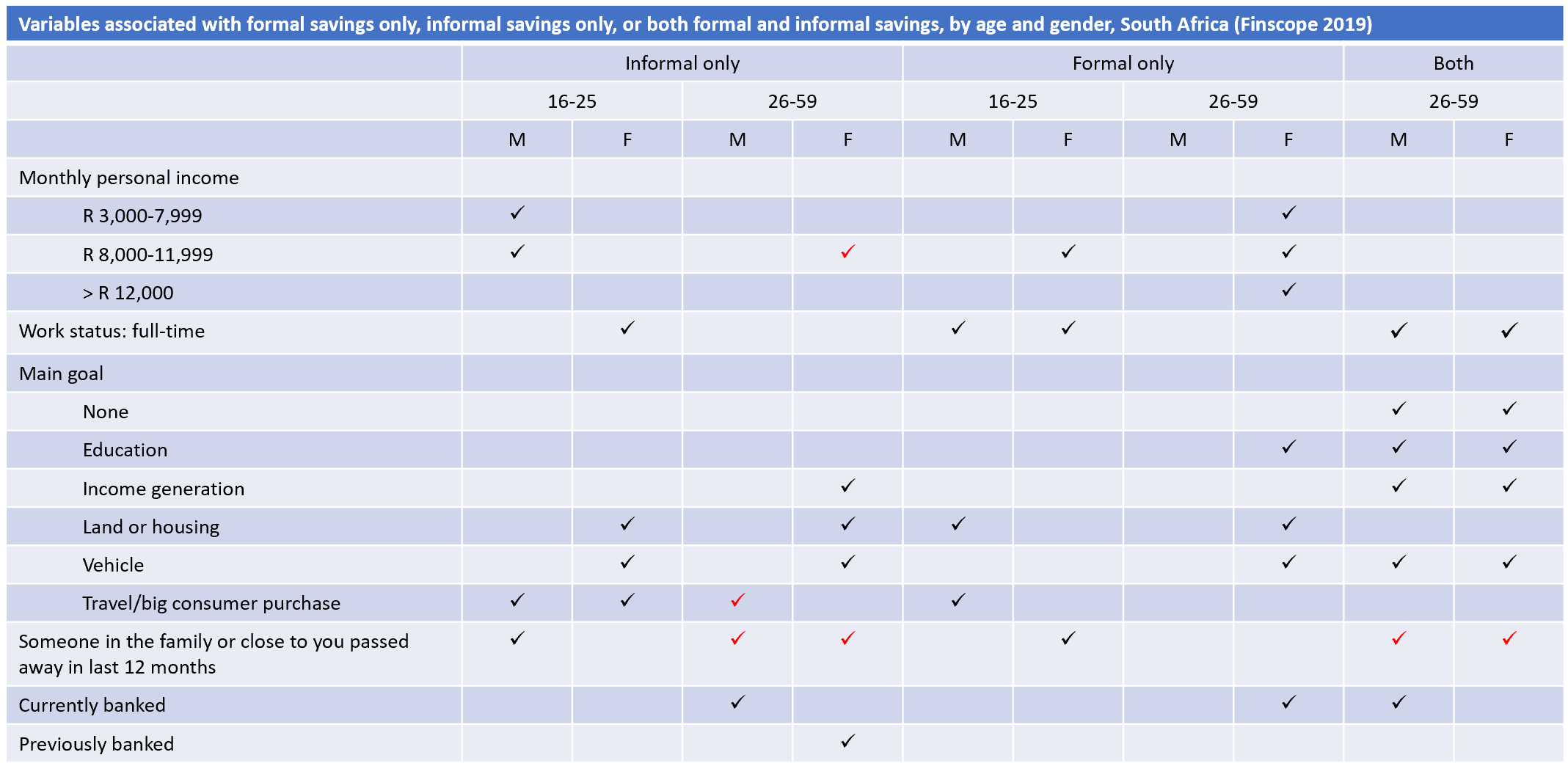

In South Africa, data trends led us to look at larger age ranges: 16 to 24 and 25 to 59. Here too, income, employment and goals influenced the likelihood across all age groups of having formal savings, informal savings or both. This influence was particularly pronounced for women.

Other interesting patterns also emerged. For example, the loss of someone close was associated with different types of savings among women and men ages 16 to 24. Similarly, women ages 25 to 59 who were currently banked were more likely to use formal savings, while women in the same age group who were previously banked were likely to use informal savings. What the data does not tell us is whether this latter group left the banking system proactively because they prefer informal services or reluctantly because formal products were not meeting their needs.

Variables associated with saving in South Africa

The limits of mining existing data

A more complete investigation into the reasons behind the patterns we uncovered will likely require quantitative analysis of other datasets, including lifestyle variables not typically covered in financial inclusion surveys and longitudinal research; a customized data gathering exercise; or deeper qualitative research grounded in the realities of context. Such analyses could be used to answer some of the many questions triggered by this research, starting at a national or regional level to capture important contextual realities. These questions include:

- How do women’s life stages affect their economic empowerment, decision-making power and perception of the value of financial services? And how do these factors shape their use of formal vs. informal financial services?

- Why do women’s rates of access to formal savings and other services start out higher than men’s at a young age but then plateau at a much lower level?

- Do behavioral differences among older and younger cohorts reflect permanent generational change, or will the behavior of younger cohorts begin to resemble that of their predecessors as they age?

- How does complementarity play out in the gendered use of formal and informal financial services, and how can it be strengthened?

- Which features of formal savings products or aspects of the customer journey are making women switch to informal savings?

Existing financial inclusion datasets may not provide complete answers to these questions, but gender-disaggregated analysis has shown that there are more clues buried in the data than the industry has yet leveraged.

Related Blogs

Driving Change: Hello Tractor and ABERA

CGAP, IDH, FSD Network & FSD Kenya are working with Hello Tractor as part of ABERA, which empowers rural women in agriculture. We aim to address gender and climate challenges while strengthening Hello Tractor's business and financial service links.

Maximizing the Impact of Financial Inclusion for Young Women

Among which segments of young women could investments in improved financial services make the most impact? We highlight findings from a recent CGAP segmentation exercise.

Add new comment