Interoperability and Customer Value

Whether booking an airline ticket, making a telephone call or performing a banking transaction, interoperability exists almost everywhere in our daily lives. The ability for systems to connect and work together allows for e-mails that pass effortlessly around the world and trains that travel between cities no matter who laid the tracks. Yet interoperability remains largely absent from the financial services used most frequently by the poor.

Today’s mobile money services have been created and scaled as closed-loop networks, often connected only bilaterally or through third-party aggregators to achieve limited forms of interoperability. These limited, uncoordinated approaches to interoperability have created inconsistent customer experiences and often fail to deliver essential, pro-poor elements of digital payment systems.

The most obvious benefit of digital financial services (DFS) interoperability is that it allows customers to transact freely without worrying about compatibility issues. However, the value proposition of interoperability goes beyond customer convenience. Interoperability helps to create the efficiencies and scale in DFS that make the other benefits of going digital possible. While data on DFS interoperability remains limited, three hypotheses underpin how CGAP believes interoperability can unlock the potential of DFS and advance financial inclusion.

Hypothesis 1: Interoperability encourages existing customers to transact more.

Metcalfe’s Law, a principle dating back to the communications networks of the 1980s, states that the value of a network grows at the square of the number of connected users. Put simply: network effects matter. Data from the history of today’s SMS and ATM services prove this theory as it relates to telecommunications and traditional payment networks.

A similar rationale implies that DFS interoperability has the potential to grow the volume of transactions by better connecting existing customers. Transactions that may have previously been made using cash can move more easily to digital. However, it should be noted that the walled gardens of today’s mobile payment networks already have cracks. SIM swapping, over-the-counter/voucher transactions (i.e., using an agent to intermediate) and aggregators already allow account holders at different institutions to transact with each other, though typically with increased cost and difficulty.

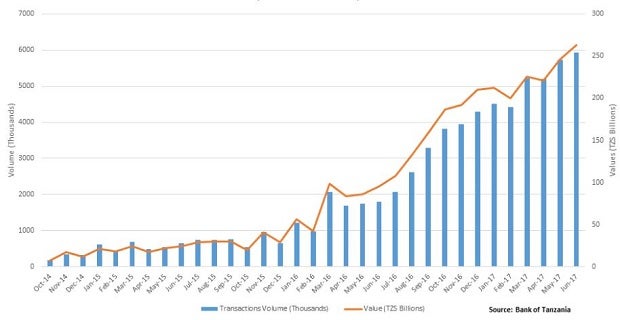

One early data point is Tanzania. Since surcharge-free person-to-person (P2P) transactions became available between major providers in 2014, the market has seen significant growth in transaction volume across networks. Payments between services now total approximately 5 million transactions per month, or 30 percent of all P2P transactions in the market. However, more granular data are needed to fully answer the question of how different types of transactions have been impacted and the extent to which interoperability has driven overall growth in the market.

Hypothesis 2: Interoperability promotes new ways for users to transact.

Most DFS interoperability arrangements have focused, at least initially, on P2P payments. Mobile money industry schemes in Tanzania and Uganda, DFS payments through Pakistan’s 1Link switch and the PesaLink scheme created by banks in Kenya are a few examples. However, interoperability may offer still greater value by promoting DFS uses beyond remittances.

Retail payments are one such use. Imagine if your credit or debit card was accepted only by merchants who happened to share a relationship with the same bank who issued your card. This is the case for DFS merchant payments in most developing markets today. Providers are attempting to grow merchant networks as their proprietary networks work against them. The sheer scale needed for merchant acceptance may make DFS retail payments a difficult end-game without effective interoperability. Point-of-sale networks in most developed markets are more than 10 times the size of access point networks (e.g., branches and ATMs).

Hypothesis 3: Interoperability expands access to digital financial services.

Finally, interoperability may bring entirely new customers into the DFS ecosystem. As the scope and scale of networks expand, the overall value proposition of DFS may improve and attract untapped customer segments. Quite simply, the more you can do with mobile payments, the more people are likely to want to use them.

Yet the extent to which interoperability can grow the total number of users remains unproven. The ability to attract customers will ultimately depend on the validation of our first two hypotheses, increasing the prevalence and uses of DFS until a tipping point is reached for consumers who have not yet gone digital.

Numerous DFS interoperability arrangements are just now being planned or coming online, supported by a variety of business, governance and technology schemes. CGAP believes that only through inclusive governance, balanced economic incentives and effective technology will these schemes reach their potential. CGAP is working across markets to influence the debate and help shape rational, pro-poor solutions. We look forward to sharing our learnings in the months ahead.

Also in this Series

How Can Funders Promote Interoperable Payments?

Interoperability can make digital payments more convenient and useful for low-income customers. Find out how funders can support the development of interoperable payments systems.

Comparing India’s UPI and Brazil’s New Instant Payment System, PIX

Many countries are pressing forward with new systems to enable better, faster digital payments. Brazil's instant payment system, PIX, is among the newest and most exciting. How does it compare to India's well-known UPI system?

Add new comment