The Many Faces of Social Exclusion

Meet Aminata, a young Senegalese woman in her late teens. She lives with her parents and four siblings in Kedougou, a small town in southeastern Senegal. Aminata completed her primary education but didn’t finish high school because her parents wanted her to start earning money for the family. However, finding work was not easy for Aminata. Jobs are plentiful in the local gold mines, but these are often reserved for men and boys. She occasionally works in the cotton fields and, depending on the season, she goes to the local market to sell avocados and plantains imported from Guinea. Aminata wants to save up for a cell phone. She gives most of her income to her parents, and the money she saves is kept in a box at her house. Sometimes her father lets her use the family cell phone, but usually he keeps it out of her reach because he thinks she’ll engage in frivolous activities. In many ways, Aminata’s parents and one of the village leaders have a strong influence on her aspirations and limit her access to information and services like health care.

Aminata’s story is not unique. Despite progress around the world, many people continue to face limited access to social and economic opportunities. While not a cure-all, financial services have the potential to connect them to more opportunities. Evidence shows that financial services have a direct impact on health, education, gender equality and food security. If more meaningful progress is to be achieved in the future, we need a deeper understanding of the many other ways financial services might intersect with social exclusion. This includes uncovering which specific groups are socially and economically excluded, asking why and how they are excluded, and identifying where financial services can have the biggest impact on people’s lives. In Aminata’s case, her family and religious leader play a strong role in her life. Do they influence her ability to open a savings account? How is her larger social network affecting her understanding of financial services? And should potential solutions for women like Aminata account for these particular social exclusion factors?

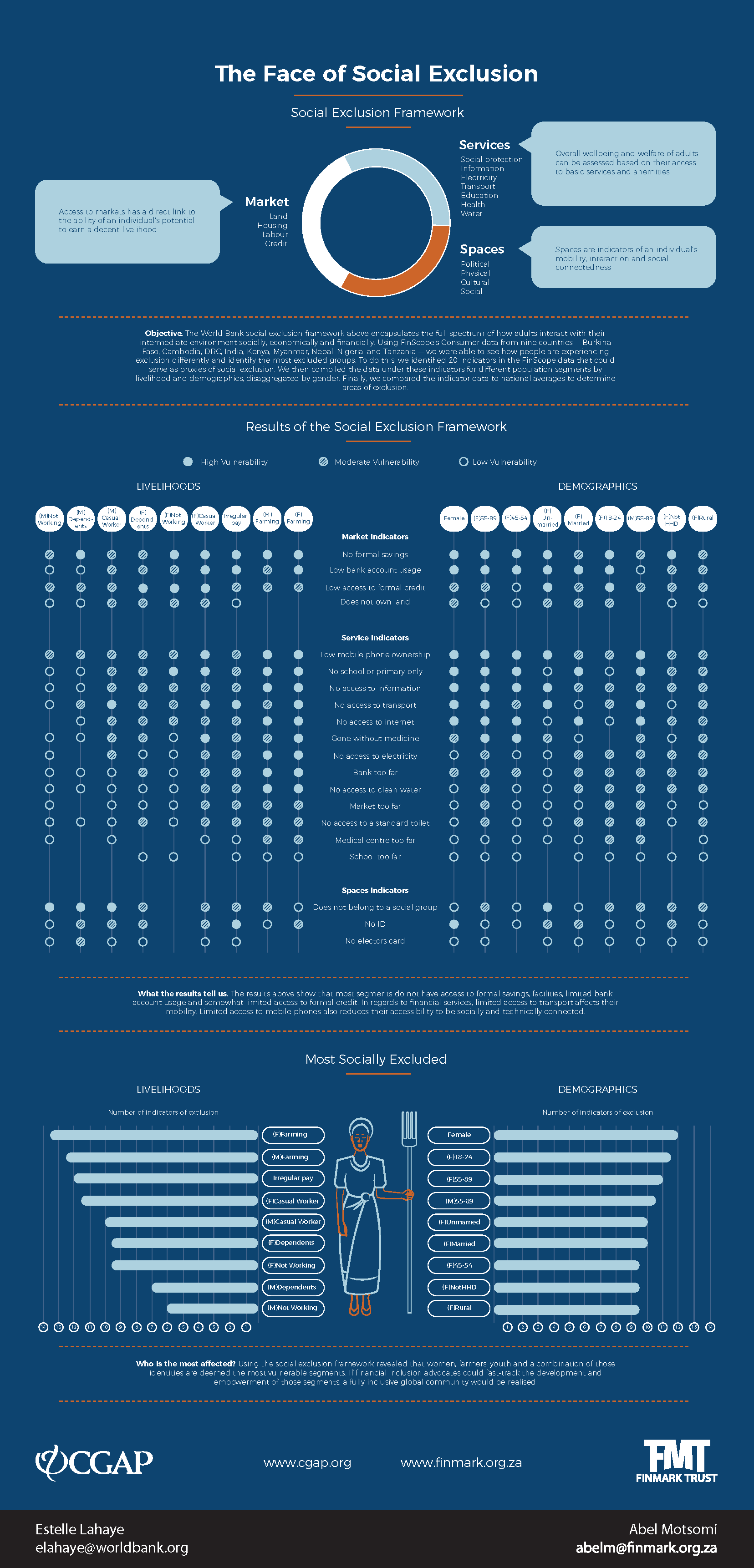

Because CGAP is interested in social and economic exclusion, we partnered with FinMark Trust to start exploring these issues for both demographic and livelihood segments. For each segment, the analysis begins to uncover particular areas of exclusion that may deserve further consideration by the financial inclusion community. The data show that women above 55 years old have limited access to basic services such as electricity, clean water, sanitation or transportation, more so than their younger peers. This is clearly an area that should be prioritized since financial solutions can enable access to these essential services. Additionally, access to these services can impact other areas of exclusion. CGAP’s “Escaping Darkness” report on pay-as-you-go (PAYGo) solar energy, for example, shows that one of the main reasons poor, often geographically isolated people invest in PAYGo is to be more connected to the world through devices like TVs. In the words of one customer in Cote d’Ivoire: “I like solar because it gives me access to information. That’s it.” The infographic below shares some insights from our analysis with FinMark Trust and shows that social exclusion has many facets and faces.

This analysis is a starting point to help decipher where the financial inclusion community's attention should be. It doesn’t uncover the complexity of the lives of these different segments, but does offer direction for future exploration. It is also clear that the segments are not one dimensional and that the intersection of age, livelihoods, location and gender influence the types of social exclusion people experience. For example, the experience and aspirations of young women working occasionally will likely differ from those of elderly women working on a farm. Country context also matters. As the financial inclusion community delves deeper into understanding different segments, it is important to grasp the layers of their complexities and turn this knowledge into tailored solutions, whether the solutions rest with providers or policy makers.

Add new comment