Measuring Women’s Financial Inclusion: The 2017 Findex Story

The 2014 Findex data was a wake-up call to many actors in the financial inclusion space. Despite important progress, the global gender gap remained at 7 percentage points globally and 9 points for developing countries.

Since 2014, we have seen many calls to action and important efforts to address the gender gap. Alliance for Financial Inclusion (AFI) members signed the Denarau Action Plan, which is committed to halving the gender gap by 2021. Of the 40 AFI member countries that have financial inclusion strategies, 27 made gender-specific commitments in their financial inclusion strategies. More recently, donors such as the Bill & Melinda Gates Foundation increased their funding and commitments to women’s financial inclusion, recently launching an institutional gender strategy. And CGAP joined forces with Women’s World Banking, AFI, CARE and over 200 other organizations in a community of practice to share ways of tackling remaining bottlenecks.

The release of the 2017 Findex data gives us an opportunity to measure our collective progress since 2011 and identify where new initiatives should focus. What does the latest data show us?

The gender gap in account ownership persists

While more men and more women own financial accounts than ever before, the gender gap remains unchanged at 9 percentage points for developing countries. From 2014 to 2017, men’s account ownership in these countries increased from 60 to 67 percent, and women’s ownership grew from 51 to 59 percent. Yet the headline gender gap masks important gains made in many economies. In India, for example, the gender gap dropped substantially from 20 to 6 percentage points between 2014 and 2017. The headline gap also obscures important markets such as Indonesia, where more women (51 percent) than men (46 percent) now have access to accounts.

Gender gaps in many economies are slowing overall progress

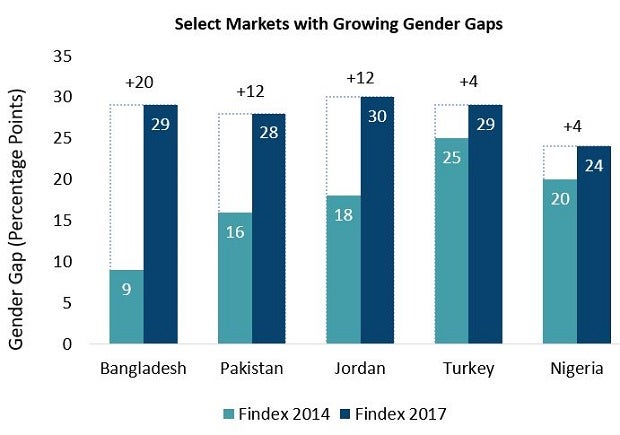

Several countries have made important leaps forward in financial inclusion but have not done enough to address the barriers that prevent women from accessing and using financial services. As CGAP CEO Greta Bull mentioned in her commentary on Findex, women’s access figures have dragged down the overall figures in these countries. Bangladesh and Pakistan stand out as places where growing gender gaps have accompanied gains in financial access. Bangladesh now has one of the largest gender gaps in the world at 29 percentage points, followed closely by Pakistan at 28 points.

Mobile money is closing the gender gap in many, but not all, African countries

Mobile money is helping women to accelerate their access to the formal financial system in many Sub-Saharan African countries. In Cameroon, Gabon, Kenya, Liberia, Mali, Mozambique and Zimbabwe, the gender gap in mobile money access is significantly smaller than the gap in bank account ownership. In a few markets like Chad, Cote D’Ivoire, Ghana and Uganda, there is a limited difference between bank account and mobile money access for women, indicating that perhaps a different set of barriers is limiting women’s ability to access the formal financial system. It is important to note that some large markets, such as Ethiopia and Nigeria, have yet to see important gains from mobile money because they have not fully embraced an enabling environment for digital financial services.

Mobile money appears to be widening the gap in a few markets. In Bangladesh, the 22 percentage point gap in mobile money is higher than the 18-point gap in bank accounts. Iran, where 94 percent of adults own an account, also shows a higher gender gap in mobile money (9 percentage points) than in bank accounts (4 percentage points).

Government policies are likely driving progress, as in the case of India

India’s Unified Payments Interface and government-driven efforts to help women obtain basic accounts appear to be behind the substantial drop in the country’s gender gap between 2014 and 2017, from 20 to 6 percentage points. Women’s access to bank accounts increased from 43 percent in 2014 to an impressive 77 percent in 2017. Of course, access does not equate to use, and India’s account dormancy rates are nearly double what they are in other markets. More research is needed on how to make women more active participants in India’s financial system.

What does this mean going forward?

Findex 2017 paints a mixed picture on progress to eliminate the gender gap in financial inclusion. Perhaps the financial inclusion community has prioritized the wrong barriers. For example, mobile phone ownership was widely purported to be a stumbling block for women’s access and use of mobile money. But data from Findex and a recent CGAP paper analyzing Gallup data show that women’s phone ownership is much higher than previously thought, with over 81 percent of women globally owning a mobile phone. Or perhaps we have not sufficiently addressed barriers that vary greatly across economies, such as cultural norms, which are likely driving the lag in mobile account ownership for women, particularly in markets like Bangladesh. Issues like literacy, digital literacy and harassment by male agents are among the issues that warrant more attention.

At the policy and regulatory level, central banks often assume that their initiatives are gender neutral. In reality, policies and regulations significantly impact women’s financial inclusion. Women, Business and the Law’s 2018 database measures discriminatory policies and laws across economies. It shows that Jordan and Pakistan, where just 27 percent and 7 percent, respectively, of women are financially included, have policies that undermine women’s ability to join the workforce and own and inherit assets — important barometers for women’s desire and ability to participate in the economy, including their use of financial services. Cases like these suggest that many countries should focus on adopting policies within and beyond the financial sector that address barriers to women’s economic inclusion.

Findex is truly a treasure trove of information. I encourage everyone to dig deeper into the data and identify which policies are driving women’s uptake and use of financial services.

Also in this Series

Pakistan Enigma: Why Is Financial Inclusion Happening So Slowly?

Just 21 percent of adults have accounts in Pakistan, despite decades of support for financial inclusion. What could accelerate progress?

India Moves Toward Universal Financial Inclusion

The 2017 Findex shows India has made significant financial inclusion progress in the past four years, but use remains a challenge.

Add new comment