5 Ways Gender Lens Investors Can Deepen Impact on Financial Inclusion

Gender lens investing (GLI) is becoming a more popular way to invest in financial inclusion. As we argued in an earlier blog post, there are three specific opportunities for GLI investors to help meet women’s financial needs: supporting women entrepreneurs, investing in sectors that predominantly employ women and addressing women’s consumer needs. But how can GLI funders set themselves up for success and maximize their impact while working in these areas? Below are some recommendations based on CGAP’s review of the GLI literature and interviews with stakeholders, including impact investors, development finance institutions, donors, GLI networks and platforms.

1. Improve impact measurement efforts

GLI is still nascent, and although the business case for investing in women is proven, there is still a need to build the evidence base for impact. To build a meaningful evidence base, performance indicators should go beyond outputs to identify outcomes and to chart impact pathways for GLI investments. There have been efforts among investors and GLI initiatives to align indicators and metrics to enable the measurement of results from GLI investments, but further collaboration among stakeholders is needed.

For example, the 2X Challenge developed specific criteria that determine what qualifies as a GLI investment, while the Global Impact Investing Network (GIIN) developed the IRIS+ indicators to measure the gender impact of investments. The 2X Challenge and the GIIN are now collaborating to harmonize GLI indicators and have joined forces to set out a series of key gender impact indicators, aligned to the 2X Challenge criteria, which is a welcome development. GLI funders are at different stages of carrying out impact reviews. More collaboration among funders and other stakeholders could enable the collection of hard evidence underpinning the effectiveness of the GLI approach. This collaboration could be in the form of a knowledge repository or platform with aggregated data and information on benchmarks, impact studies and other evidence on GLI. This would help improve the rigor with which impact is being measured, such that women are truly benefiting from financial products and services designed for them.

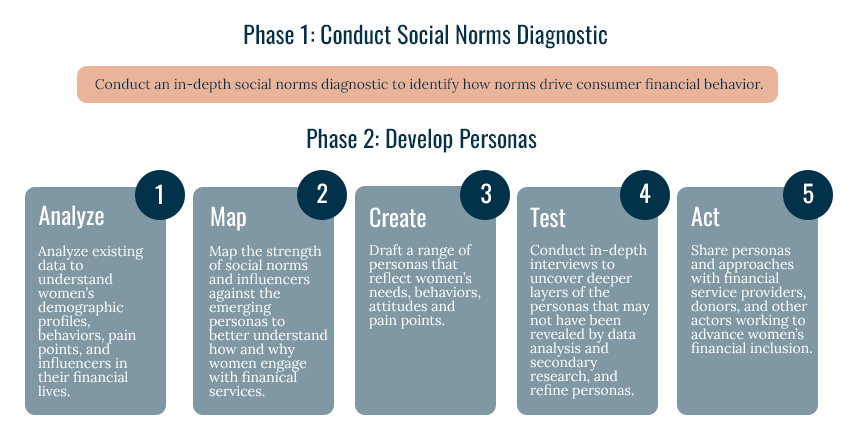

2. Consider the influence of social norms

GLI requires a gender analysis at the beginning of every investment decision. However, few funders examine the impact of social norms in conducting this analysis. Social norms are the rules and accompanying behaviors that govern social behavior, perceptions and conduct. Among development funders looking to address women’s financial inclusion, there is consensus that social norms play a role in driving the financial inclusion gender gap. This is part of a broader discourse on the framing of women’s empowerment and the underlying factors determining its achievement.

GLI investments for women’s financial inclusion primarily aim at addressing women’s access to capital for entrepreneurship. Social norms around women’s ability to own businesses and assets, and their ability to work outside the home, could affect the uptake of solutions backed by these investments. Funders should seek to carry out social norms diagnostics as part of their gender analyses. They should further incentivize and encourage providers and investees to consider and address social norms as they run their operations and develop products and services for women.

3. Leverage sex-disaggregated data

To enhance the value proposition of financial services for women, GLI funders can encourage investees to become more customer centric. Such an approach puts customers — in this case, women — at the heart of solutions, builds on insights about their lives and creates institutional culture, capacity and processes that provide long-term value for customers.

To do this, sex-disaggregated data is integral in understanding women’s needs and behaviors, which thereafter informs the nature of solutions, products and services that truly meet their needs. Yet today many providers do not have such data or do not use it when it is available. For example, a recent report from the Financial Alliance for Women showed that while 80% of fintechs surveyed can disaggregate data by sex, most do not use such data. This calls for GLI funders to carefully identify investees who are committed to advancing women’s financial inclusion and are willing to explore the use of data to achieve this goal. Subsequently, GLI funders can leverage their equity investments and board positions to drive organizational change management and provide capacity building and technical assistance to investees.

4. Strategically fund new business models likely to have impact and reach scale

By leveraging technology, fintechs can bypass inflexible requirements for women (e.g., lack of ID or collateral) that traditional financial services providers are not able to. These new models present an attractive funding opportunity. For example, 40% of the GLI private funds invest in fintechs.

To achieve impact and business potential, funders should take into account a fintech’s stage of development in structuring their funding. CGAP’s research into investments in fintech solutions shows that funding from both commercial investors and development funders targets mature companies with proven business models, such as payment wallets and digital credit. These investments can have impact if they are used to help fintechs take their products to financially excluded or underserved populations, such as women; but without data on customer outcomes, the jury is still out. In contrast, funding for more diverse or riskier innovations that could benefit women is more difficult to find. Funders with a stronger impact mandate and a higher risk appetite can take the lead in supporting new and impactful investees, in both customizing their solutions and developing their operations. Additionally, blended finance could be used to test and prove innovations, thereby helping prepare investees for GLI investments as well as making GLI funders confident with their investments.

Realistically, however, fintech alone is not sufficient to resolve the financial inclusion gender gap. As discussed above, a focus on understanding social norms and customer centricity in product design and delivery is required.

5. Develop an enabling environment for investments

There are wider ecosystem challenges and barriers that prevent the uptake of some of the solutions aiming to address women’s needs for financial services. These include regulations, payment systems infrastructure, and identity systems and requirements. These can heavily affect the impact of GLI investments for women’s financial inclusion. GLI funders should seek to understand these challenges and work collaboratively with market actors to address them. As a start, GLI funders can support policy and regulatory reforms, payment infrastructure changes and identification systems, as well as conduct market research, to better understand the investing ecosystem within a given context.

There are many considerations and opportunities for optimizing the impact of GLI investments for women’s financial needs. Collaboration among GLI funders can go a long way toward addressing the challenges, advocating for best practices and streamlining actions in the GLI space.

Do any of the opportunities and considerations resonate with your organization? Contact Estelle Lahaye here and let us know how we can help.

{kind=link}

Add new comment