Could e-Commerce Bring Women’s Financial Inclusion in Bangladesh?

In financial inclusion, we often focus on closing the gender gap in account ownership as a means of empowering women. Yet, as many have pointed out, accounts by themselves do not lead to empowerment. Unless having a financial account comes with a compelling reason to use it, most women will not use their accounts to capture opportunities. Fortunately, even in countries where many women are financially excluded, women’s financial behaviors tell us a lot about what use cases may help to empower them. In Bangladesh, there seems to be an opportunity to empower women through e-commerce or an informal variant of e-commerce that is especially popular among women.

The e-commerce market in Bangladesh has experienced significant growth over the past five years. A 2018 pi STRATEGY study found that e-commerce increased from $25 million in 2014 to over $200 million in 2017. This study forecasted that online sales will reach $1 billion by the end of 2021. Currently, according to the e-Commerce Association of Bangladesh (e-CAB), an average of nearly 25,000 orders are placed online every day. The e-commerce market is growing especially fast in rural areas; in 2017, e-commerce grew 127 percent in urban areas and 167 percent in rural areas.

While there are no concrete, gender disaggregated statistics on e-commerce use in Bangladesh, it is estimated that an overwhelming majority of online shoppers and entrepreneurs are women. The Daily Star, a leading newspaper in Bangladesh, stated in a March 2018 article that women dominate the e-commerce market of the country both as shoppers and entrepreneurs. Biplob Ghosh Rahul, the CEO of a product delivery company called eCourier that fulfills online orders, indicated in the article that women run 73 percent of its 5,000 registered businesses.

“Definitely women are leading the [e-commerce] industry – there’s no confusion about it,” Rahul said.

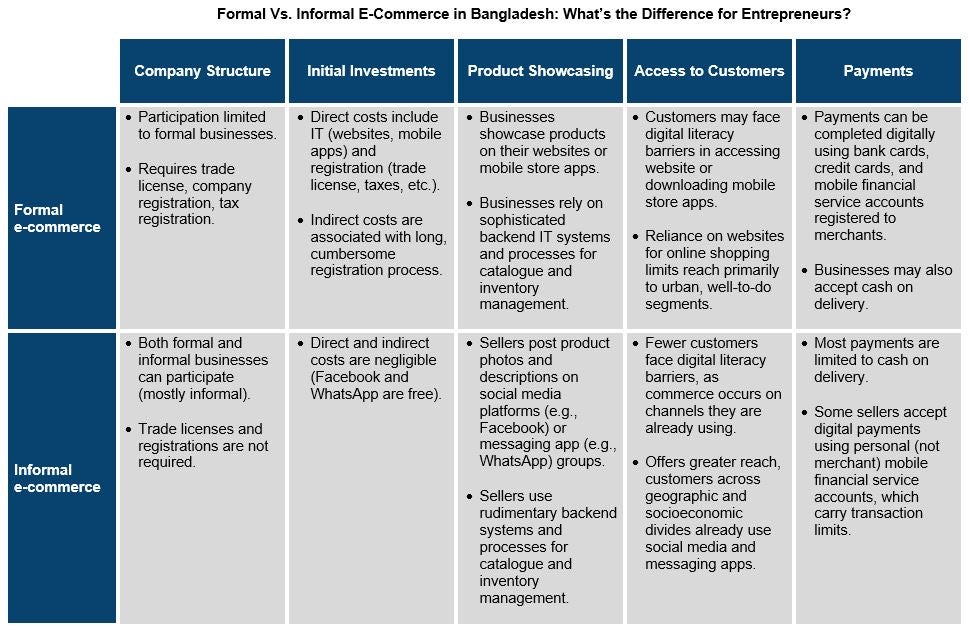

Yet e-commerce presents barriers to entrepreneurs in the informal sector, where many women are concentrated. To transact on e-commerce platforms in Bangladesh, businesses need their own bank accounts, and to obtain a bank account, they need to be officially registered with the government. However, a director at e-CAB says that many Bangladeshi entrepreneurs operate their businesses informally on Facebook, without a business registration. The long, cumbersome process of obtaining a trade license deters many, and cultural norms can make it especially difficult for women to go through the registration process on their own. As a result, a large percentage of female e-commerce entrepreneurs operate small enterprises within the informal sector and opt to use an informal variant of e-commerce that better meets their needs.

Unlike classic e-commerce — where product showcasing, order placement and payments are done over electronic channels, such as websites and mobile apps — informal online commerce occurs when product showcasing and order placement are done on platforms such as Facebook, Instagram, WhatsApp and Viber while payments are mostly done through cash-on-delivery. Relying mostly on cash-on-delivery enables informal businesses to bypass the requirement for a business registration.

The growth of informal online commerce has also provided female entrepreneurs with enormous opportunities because it allows them to work at their own pace from their homes and requires low initial investments. It helps women overcome some intrinsic cultural barriers with respect to limited mobility on their own, safety and security issues that adversely affect their labor force participation (which, in Bangladesh, is 36 percent for women and 80 percent for men, according to labor statistics). Being able to operate businesses from home directly addresses this barrier.

Research is beginning to shed light on why so many female shoppers engage in informal online commerce. In late 2018, a CGAP-supported pi STRATEGY study interviewed women in Bangladesh and found that this type of e-commerce has become a preferred way of shopping for women because of its ease, convenience, product variety and price. All female respondents in this study who were asked about their views on buying things online expressed interest in making online purchases.

“The cosmetics shop in our local bazaar has maybe 10 different types of lipsticks; the Facebook page I bought cosmetics from last Eid had over 100 varieties of lipsticks at a wide range of prices. But it took about a week to receive my orders from the Facebook page. I don’t like the wait,” said one 24-year old woman from a semi-urban town.

Overall, informal online commerce connects entrepreneurs and shoppers across urban, semi-urban and rural markets and, therefore, opens up significant market opportunities that were previously unavailable.

Literature on women’s financial inclusion shows that women have very complicated financial lives. A 2018 Women’s World Banking report on Bangladesh indicated that women are in charge of saving for emergencies, meeting health expenses, paying school fees and planning for the future. The informal online commerce opportunity in Bangladesh is an example of a use case that addresses women's needs for income generation on the supplier side and safety and convenience on the buyer side. Current digital financial services meet short-term person-to-person transfer needs, but finding innovative mechanisms to link mobile money wallets to informal commerce platforms could go a long way toward nudging a large segment of shoppers and entrepreneurs into the world of digital payments. This could get them on the first rung of the financial inclusion ladder — an account to be used for payments — while building the foundation from which other use cases, such as digital credit, could emerge.

The gender gap in financial inclusion cannot be reduced solely by expanding women’s access to accounts. Those accounts must be tied to compelling reasons and opportunities to use them. This can catalyze sustained financial inclusion for women. And that is real empowerment.

A supplement paper to this blog post can be found here.

Related Blogs

Climate Resilience Through Financial Services: Farzana’s Story

Women, especially those in low-income countries, are faced with higher risk, greater vulnerability, and fewer tools to cope with the impacts of climate change. Financial services can empower women to manage climate risks and build resilience.

Maximizing the Impact of Financial Inclusion for Young Women

Among which segments of young women could investments in improved financial services make the most impact? We highlight findings from a recent CGAP segmentation exercise.

Comments

Very insightful blog post…

Very insightful blog post. Really loved the table summarizing the difference between formal and informal e-commerce in Bangladesh and i most say this is also true looking at the Cameroonian e-commerce landscape. giving its transaction costs and limits (5/day; 15/week; 40/month), sellers find it difficult use their personnal mobile money accounts (not merchant) as payment mechanism. Orange Cameroon recently introduced an alternative feature called "Small Business Partner" that enables sellers to receive up to 200 transactions/month at a special pricing. The registration process that gives access to such mobile money accounts is very simple but much is yet to be done to enable small entrepreneurs effectively adopt mobile money as a payment solution for their income generating activities!

Add new comment