Financial Inclusion for What?

Within the financial inclusion community, there are growing efforts to review our understanding of what makes financial services valuable for poor people and the longer-term outcomes that the use of financial services can help them achieve.

This soul searching is motivated by recent assessments of what has been accomplished to date and the remaining challenges. The global financial industry has enabled access to financial accounts for millions of financially excluded people in recent years. While taking stock of this achievement, the industry is now confronted with the fact that low usage and inactivity has kept dormancy rates persistently high. This is especially true across Africa and India, where some of the highest growth rates in account ownership are found.

This growth in access is accompanied by reviews of rigorous studies around the world that find mixed, sometimes contradictory, evidence on the impact financial services are having on several indicators of financial well-being.

In this context, the financial inclusion community is being forced to ask: “Financial inclusion for what?”

This question has certainly been the motivation behind CGAP’s work over the last two years to re-imagine the impact narrative for financial services. Based on our review of the global evidence, this blog shares early insights identifying specific outcomes that poor people can achieve thanks, in part, to the use of financial services. It also highlights various knowledge gaps that the financial inclusion community should address to better understand what makes financial services more useful for poor people and positively impacts their well-being.

As Greta Bull points out in her recent blog post, "Keeping Our Eyes on the Prize in 2020," we began this work by asking one question: “What matters to poor people?” In our search for answers, we looked broadly at development literature beyond the financial inclusion space to document the various intermediate and longer-term outcomes that poor people seek to achieve greater well-being. Only then did we turn our attention to examining evidence on whether financial services help poor people attain these desired outcomes.

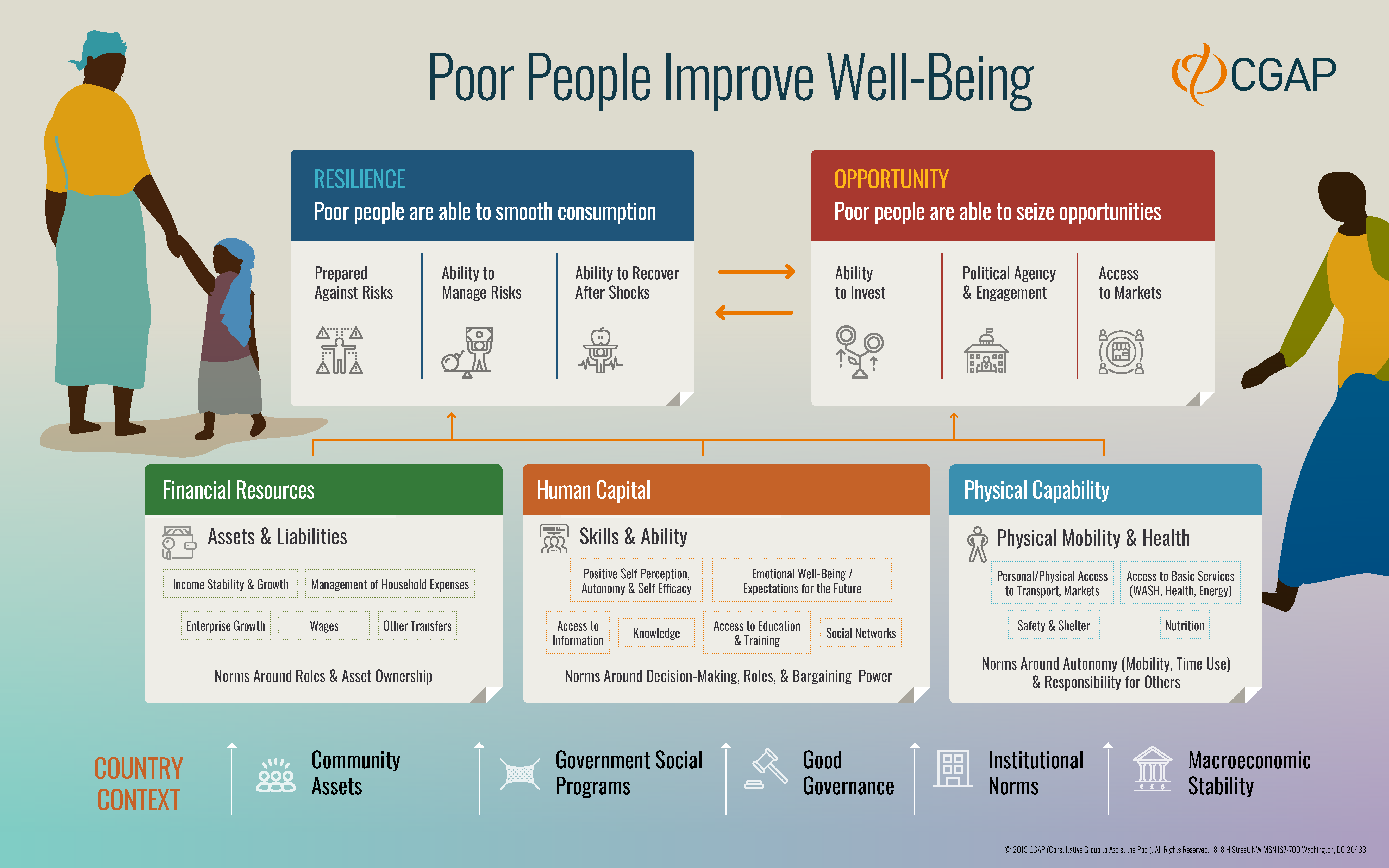

As it turns out, the evidence consistently shows that poor people use financial services to help them achieve two intermediate outcomes on the way to improved well-being: building resilience and capturing opportunities. As explained in our impact narrative, “building resilience” refers to people’s ability to prepare against risks, cope with shocks when they occur and recover after shocks, all of which smooths their consumption. “Capturing opportunities” refers to people’s ability to seize investment opportunities that improve their livelihoods.

We have identified in the literature a dynamic cycle between building resilience and capturing opportunities that is central in our analysis to identify key knowledge gaps. Resilience gives people the confidence to take on riskier but more rewarding investment opportunities. If captured, these opportunities further improve people’s resilience, which in turn, allows them to set their sights on investment opportunities that were previously unreachable. When these are captured, resilience improves even more — and so forth, in a virtuous spiral where resilience levels and opportunity sets improve and lead to greater well-being. (Conversely, when people suffer shocks strong enough to break their resilience level, they can go downward in the spiral.)

This dynamic framework implicit in the literature suggests more tangible outcomes from the use of financial services at any resilience level. People can use financial services to capture a new set of opportunities that seem mainly related to three future outcomes:

- Greater financial resources. Poor people use financial services to build assets and manage liabilities. For example, financial services can help households smooth and increase income, manage expenses, invest for enterprise growth or better employment, or transfer money used to cope with shocks or invest.

- Better human capabilities. Poor people also use financial services to build useful skills and acquire knowledge. For example, digital financial services have been shown to simplify the process of paying for education and training. The use of financial services can improve people’s perceptions of their own capacities, their autonomy and their expectations for the future. The use of financial services can also imply socialization with other people that can help build social networks, encourage positive self-perceptions and access to information and knowledge.

- Better physical capabilities. In addition, poor people use financial services to improve their health and physical mobility. Evidence shows that digital financial services make it easier to pay for basic services; build water, sanitation and hygiene infrastructure; and use health care services. Financial services can also enable access to better food and nutrition, transport services, electricity and better housing or shelter.

However, our analysis of the global evidence also reveals three key knowledge gaps regarding exactly under what circumstances financial services can or cannot contribute to these future outcomes. These gaps currently limit the effectiveness of financial inclusion programs and policies, as well as our ability to learn from past successes and failures:

- The industry innovation gap. There are specific financial services whose sizable positive impact toward future outcomes is most consistent in the literature. These include savings and insurance. Payments also fall into this category, although the positive impact from payments appears to be lower than the impact of savings and insurance. However, even if we know that these services can have a positive impact, it remains a challenge to get the financial industry to develop viable business models to deliver them to poor people at scale. Formal financial services providers have struggled to devise sound businesses models for offering savings and insurance services to more low-income customers. Formal payment services have reached the poor at a much greater scale but still exclude most people in rural areas. Therefore, policies and initiatives that aim to spur industry innovations to viably deliver savings, insurance and payments to poor people seem to be on the right track. The question of how to effectively foster innovation, including the roles of public and philanthropic capital in different market contexts, remains an open one.

- The impact knowledge gap. For other types of financial services, like credit and pay-as-you-go (PAYGo) services, the impact evidence is mixed or scarce. In the case of credit, despite the large number of studies over time, there is a persistent need to better understand the context in which credit can have positive, neutral or negative effects on future outcomes, as most studies do not identify the product, client or market conditions that lead to the observed impact results. For PAYGo solutions, some evidence points to differing ways in which these services bring value to poor people’s lives, but further research that clarifies under which conditions positive impact happens would be helpful before deeper engagements with the industry are made.

- The research methodology gap. The research community has made great progress in the past 20 years, not only in the number of impact studies conducted around the world, but also on the methodology used to measure impact. The more recent and influential randomized controlled trials (RCTs) represent a methodology that has provided more clarity and confidence on impact estimates obtained in any given study. However, as hinted in the impact knowledge gap, there is still debate on how exactly the estimated impact happens for poor people. The contextual characteristics that shape the observed impact remain poorly understood. This is important because unlike the vaccines or clean water, which do the same job in the same way for everyone, financial services are tools that people can use very differently depending on the person’s goals and context. Developing and applying better research methods that can systematically identify contextual factors that determine a given impact will provide greater clarity on which services are most appropriate for different demographics and situations. Advances in mixed research methods are promising, and initiatives that support and test such innovations in research methodology have potential to address this gap.

In the following months, CGAP will launch a consultative process to propose a learning agenda for the financial inclusion community. This agenda will go into more detail on these knowledge gaps and how the community could address them. We hope this helps us to more confidently answer the question, “Financial inclusion for what?” and promote policies that make financial services more useful for poor people.

Also in this Series

Finance Fit for Opportunities and Shocks: What Helps Poor Clients Most

To better understand the impact of financial services on people's lives, providers will need to invest in deeper customer research with the help of the broader financial inclusion community.

Measuring the Influence of Financial Services on Reaching the SDGs

Learn about UNCDF Impact Pathways, a tool to measure the influence of digital financial services in reaching the SDGs, in this guest blog.

Add new comment