Merchant Acquiring: Why Winning Is the Wrong Approach

If digital financial services (DFS) providers are to make serious inroads on merchant payments, it is becoming increasingly clear that acquiring models need to change. Thus far, the big providers (read mobile network operators) have been all doing what they are used to doing: setting up proprietary networks of merchants to grab real estate in the market and become the dominant brand in the space. Unfortunately, there are several reasons why that’s a poor strategy to succeed in merchant payments — for the industry as a whole as well as for individual providers.

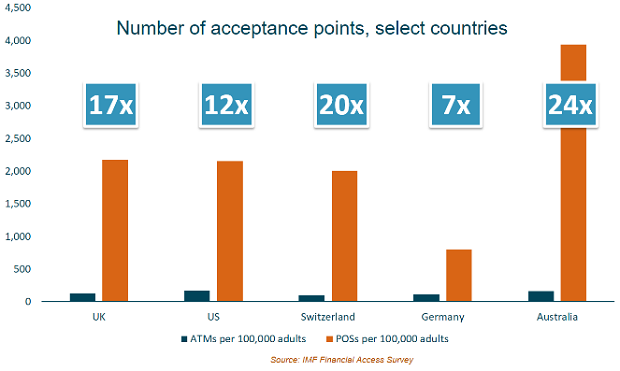

The simplest reason is scale. While customers’ need for cashing in and out might be met with agent networks that ensure a presence every few blocks, to be relevant in retail payments providers need to be present at multiple locations on virtually every street. Looking at bank cards in developed economies, there tend to be at least ten times as many point-of-sale devices where people spend money as there are ATMs where people cash out. While this comparison isn't perfect, it is probably good enough for a ballpark estimate of what providers would need to achieve in developing economies. Thinking about how often people retrieve cash versus pay for something in a retail transaction, 10x might even be a conservative ratio. Agent networks already give DFS providers plenty of headaches. Do they really have the stomach—and the capital—to build another sprawling distribution network, ten times larger than the one they already have?

The high cost of reaching scale is an important reason why in the card space today, banks directly acquire only a small share of retailers, relying instead on a sub-industry of third-party actors to do that work for them. Cheap hardware devices like smartphone dongles have enabled players like Square to reach millions of businesses that are too small for banks to equip with traditional point-of-sale devices. Third-party merchant acquirers also compete by developing customized services and point-of-sale solutions for e.g. restaurants or multi-lane supermarkets, which banks don’t have the appetite to do.

And the scale challenge isn’t limited to the merchant network. At the other end of the card acquiring value chain, processing all those transactions also requires scale, as the economics aren’t very attractive unless you operate at high volumes. This has led to the emergence of large payment processing companies. In the United States, for example, around 70 percent of retail card payments now go through one of the country’s four largest processors.

As a result of these dynamics, most banks today are not participating in the acquiring side of card payments at all, preferring to focus their effort on the issuing side — serving their own card-carrying customers. This makes sense: There’s really no need for every bank issuing cards to also acquire merchants, since these are fundamentally different businesses. As long as there is money to be made on either side, there is no reason to straddle both.

So what does this all mean for DFS providers trying to win on merchant acquiring? It means winning is the wrong approach.

First, it seems plausible that interoperability will be necessary if providers are to have any hope of reaching the kind of scale required to get momentum behind a new retail payments solution. And if that’s the case, industry players need to plan for it right from the outset or risk painting themselves into different corners by deploying large numbers of acceptance devices with incompatible technological standards. But interoperability is not just about technology: It’s about trust, brand and a common user experience, as CGAP’s CEO Greta Bull has written about. This will require real collaboration across the industry.

Second, providers ought to not just permit and enable others to interconnect through high-quality open APIs, but actively encourage the development of third-party merchant acquirers using their own business models and accepting payments from multiple issuers. Such specialized acquirers are more likely to build truly compelling value propositions for merchants, which until now often have been sorely lacking but should not be hard to create. Different types of players and partnerships could step into that space, including forward-thinking banks—as this would be a natural evolution of the card acquiring business that tends to struggle in many emerging markets. We may be seeing the beginnings of this interest from banks and will be covering it in a future post.

Third, providers may want to consider the degree to which they even want to be in the acquiring side of the business at all, as opposed to having the merchant piece be undertaken by a combination of peers and specialized third parties. That will require payment schemes with high trust, clear rules and compelling business models to emerge—which may only be conceivable in the medium term, but should form part of the strategic vision even now.

Resources

Also in this Series

Benefits and Burdens of Digital Retail Payments

Payments providers in emerging markets could earn billions if more merchants start accepting digital payments. But what are the opportunities for poor customers?

Merchant Payments: What About the Customers?

Shifting retail payments away from cash to digital instruments will require strong buy-in from end customers, who tend to like cash. How might they be persuaded?

Comments

Curious how the writers rate

Curious how the writers rate India's payment models where non-mobile intermediaries (like PayTM etc.) have acquired merchants? There density is far more, approaching the 10x ATM already.

Add new comment