Mobile Payments Take Shape in Latin America & the Caribbean

As elsewhere in the world, cash is still king in Latin America and the Caribbean (LAC), despite the demand for digital transactions brought about by the COVID-19 pandemic. While the region attracts significant investment in fintech, e-commerce and other digital businesses, the potential to reach scale and impact in the lives of most citizens — especially excluded and underserved groups — is at risk without broad, affordable and easy-to-use mobile payments.

Mobile payments took the world by storm more than a decade ago, but the LAC region did not experience the success and traction seen in other parts of the globe. Non-bank models that took off elsewhere were, for several reasons, “dead on arrival” in LAC. This was in part due to strong bank-centered regulations and widespread presence of bank incumbents. Moreover, the demand for domestic person-to-person (P2P) payments was already being met by players such as OXXO and Banco Azteca in Mexico, postal networks such as Efecty in Colombia and bank correspondents in Brazil. Other barriers included distribution networks with insufficient coverage, lack of interoperability, poor product design and poor customer experience.

Over time, reforms across markets allowed non-banks to issue e-money, enabling diverse business models for digital payments beyond traditional bank-based accounts and debit cards. New players entered the scene, including fintechs, delivery platforms, e-commerce marketplaces, digital-first banks and others.

Throughout the last decade, a variety of business models have emerged across the region. Yet few of them have accomplished long-term, consistent success. Daviplata in Colombia and MonCash in Haiti are two successful cases worth studying. Both products represent distinct models (one powered by a bank and the other by a telco) whose stories share important similarities and prove that, while mobile payments in Latin America had the flair of a mirage a decade ago, a mirage they were not.

Daviplata (Colombia)

Daviplata is a business unit of one of the largest banks in Colombia, Banco Davivienda. It launched in 2011 as a mobile wallet for person-to-person payments (P2P), in partnership with Redeban (a payments operator). Daviplata initially operated only through feature phones using simple menus in a SIM card.

In 2012, Banco Davivienda won a government contract to disburse 1 million recurring government-to-person (G2P) payments to beneficiaries of Familias en Acción, a social program. The simplicity of Daviplata’s design, its availability in a widely popular feature-phone (the Nokia 1100) and the G2P payments contract were vital in driving its initial growth.

Years later, three actions boosted adoption of the wallet. First, the development of a smartphone app in 2016 improved user experience, increasing P2P and utility payments. Second, the development of a simple “payment key” made it easy to send payments through social messaging apps. Lastly, the issuance of a virtual prepaid card enabled Daviplata to be used in e-commerce and online purchases, locally and abroad. Additionally, the QR code linked to the account enabled Daviplata to be used for digital payments at affiliated merchants. The virtual card expanded demand for the wallet significantly since traditional bank-issued debit cards could not be used online due to fraud prevention rules (a common practice in the region).

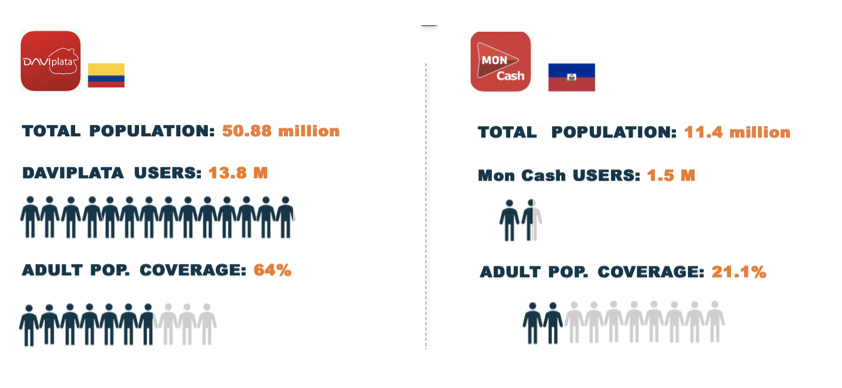

As its customer base grew, Daviplata connected to the ACH switch providing de facto interoperability with other bank accounts and wallets in the market. More recently, Daviplata opened its platform via Application Programming Interfaces (API) to provide a financial backbone to other platforms such as the Colombian deliveries unicorn Rappi via a co-branded product - Rappipay. The payments API also enabled Daviplata to appear as a payment option in different e-commerce platforms, making it available to more than 13.7 million users.

Daviplata’s pricing strategy was also key. The wallet is free, as are most transactions, and users can use the app without a data plan as Daviplata covers smartphone data costs through reverse-charge with telcos. Daviplata’s relationship with Banco Davivienda has allowed it to leverage the bank’s ATM and agent networks (over 25,000 access points), as well as offer airtime purchases, utility payments, the prepaid virtual card and other products. More recently, Daviplata added “Perfil mi negocio,” enabling small businesses to accept Daviplata payments easily, at no additional cost, and enabled Tienda Virtual to expand the wallet usage by its consumers. These features created a solid value proposition for the wallet, which closed 2021 with nearly 14 million clients — one in three Colombians — almost doubling the existing client base at the close of 2019.

But how does a free wallet make money? Daviplata generates revenue by charging third parties to disburse and collect payments from its customer base and interchange fees for processing payments through the card’s infrastructure. It plans to expand its offerings in the future to include additional insurance products, digital consumer loans and digital remittances, among others.

Mon Cash (Haiti)

In 2010, Digicel acquired Voilà operations in Haiti and later combined its own mobile money services with Voilà’s under the name Tcho tcho. Tcho Tcho offered basic payment services such as balance information, free account opening (minimum deposit of USD $2.50), deposits, withdrawals and airtime top ups. A year later, Tcho Tcho received an award from the Bill & Melinda Gates Foundation and USAID as the first company to launch mobile money services in Haiti under the Haiti Mobile Money Initiative (HMMI).

Tcho Tcho was instrumental in transferring cash to victims of the 2011 earthquake. When humanitarian transfers decreased in volume, Digicel re-focused its business strategy as well as its value proposition, redesigning Tcho Tcho.

The first step was to address the challenges and pain points experienced by Tcho Tcho customers (e.g., complex app design, lack of clarity on terms offered, etc.), as well as the difficulties experienced by customers trying to access cash (e.g., lack of liquidity of agents or insufficient agents). The second step was to reorganize and expand physical access points.

At that time, Digicel had parallel networks of agents for its business: one for the telco and one for the mobile money operation. Since these networks were not interoperable, customers ended up frustrated trying to cash out at agents that were not able to serve them. In 2015, under the name of Mon Cash, Digicel presented an enhanced service supported by a greater network of agents in partnership with Scotiabank and later with Sogebank (national policy mandates mobile money to be provided in partnership with a bank).

Through its commitment to listening to customers and conducting thorough market research, Digicel realized that P2P transfers were the product with more mass market appeal. Thus, the mobile money business roll-out needed to be adjusted. Digicel enhanced P2P transfers and expanded the offering in 2016 by partnering with FINCA Haiti to offer loans through MonCash. By 2017, Digicel had simplified its value proposition, strengthened its relations with agents – treating them as clients who needed to be understood and served – and with banks (to ensure liquidity for agents) and added a loan option. The move was a success, and by 2017, active accounts had increased from 83,000 to 795,000 and agent activity had jumped from 28% to 93%. MonCash strategy was soon expanded across the Caribbean region.

The secret to doing payments right

To be clear, if there has been a mirage for mobile payments in Latin America, it has been profitability This is compounded by the deep-rooted preference for cash in many markets. But profitability itself is not the only value these companies create. These players represent strategic investments that expand the market for the core business of their shareholders in the long run, while also benefiting consumers and other players in the market.

Daviplata and MonCash owe their success to a number of factors:

- Leveraging sponsors’ assets: Both initiatives leverage the infrastructure and services offered by their parent companies or partners – large players with established market presence in their respective markets. These organizations provide access to administrative services that reduce overhead costs, and access to physical and financial infrastructure on which payments can develop.

- Long-term vision and horizon for returns: Their investors (“parent” companies) and partners have a strategic vision and set a long-term horizon for their return expectations. The return on investment is the strategic value of those assets.

- Customers at the center: Daviplata and MonCash listen carefully to their clients. Early on, both companies identified frictions and devised strategies to remove pain points. They also realized that, in order to compete with cash, it was necessary to reduce costs or make it minimum, eliminate unnecessary steps and increase the value of clients’ money in their digital wallets.

- Constant product development:. They get their end-customer value propositions right and work consistently to improve them. Addressing users’ needs in accessible and affordable ways and continuously adding value is a focus of their business.

- Start narrow, then expand: They focused on a specific user need: P2P payments. In the case of Daviplata, once a critical mass of clients and a certain level of traction in usage was achieved, new services and functionalities were added to the wallet. In the case of Mon Cash, the focus was first on getting the core value proposition right around P2P payments, before adding loans.

- External partnerships: Both businesses leverage the capabilities of partners to expand outreach and, in the case of Daviplata, diversify revenue streams. MonCash leveraged partnerships to expand cash access points and loan offering.

- Interoperability: Daviplata's connection to the ACH ensured business expansion, not only at the P2P level but also to e-commerce, allowing its clients to have more reasons to use mobile payments instead of cash.

Ultimately, the sustainability of payments models relies on the ecosystem of digital payments that they help build. Both Daviplata and MonCash reached a large proportion of the populations in their respective markets through the factors above. But other payments services in the LAC region have garnered millions of customers too. The lessons above might shorten the learning curve and accelerate the journey for other payments players in region.

The authors wish to thank Margarita Henao (CEO, Daviplata), Ginna Vargas (Payments Manager, Daviplata) for their valuable input to this blog. A second blog will explore another payments model whose success has resulted from the combination of payments with other services to enhance their value proposition.

Related Blogs

")

How Did Bancolombia Create a Successful Rural Agent Network at Scale?

Bancolombia is a great example of a provider that's been successful in developing rural agent business models at scale, therefore playing a critical role in furthering financial inclusion. Here, we look at the factors that explain their success.

Comments

Well written blog piece. It…

Well written blog piece. It is good to see research on the Latin American financial inclusion status. In the end, LAC went digital. I would reinforce the aspect that payments have a very low margin and payment fintechs will have no other solution but to turn to side financial and e-commerce businesses to be sustainable. This is critical as margins tend to get even lower as regulators push to lower debit/credit and pre-paid card intechange fees and the expasion of interoperational instant payments systems backed by Central Banks (for example, FedNow, CODI and Pix). In Brazil, payment fintechs are becoming fully operational digital banks (such as Nubank and Pagseguro) and new fintechs are launched, sponsored by large retail chains (Magazine Luiza, Americanas and Via). While exciting news, mobile payments face issues in including the last unserved population. Low income families usually share their phones: children (distance education, streaming and other leisure activities) and adults. Thus, the phone is not always available to transact. Additionally, internet availability is still an issue, as a financial barrier (low income families often rely on public available wifi to connect) or physical (many remote areas are still not reached by reliable mobile networks).

Add new comment