Women platform workers across sectors and markets say that, on net, platforms have increased income-generating opportunities available to them – though challenges related to work/life balance, safety and long-term financial benefit remain. Tailored financial services could help women platform workers mitigate some of the downsides of this growing source of livelihood and translate new opportunities into greater security for themselves and their families over the long term.

As part of CGAP’s research on platform workers in five countries, we consulted approximately 100 women in sectors from ride-hailing to personal/home services to e-lancing. These women told us about many improvements in their livelihoods since beginning platform work. For example, 63% of women (vs. 52% of men) reported per-job income increases on platforms. Platform income also helped 59% of women to better meet daily costs, and about half to cope with the financial challenges of COVID-19. In addition, some aspects of platforms have allowed women to circumvent social and normative barriers to work, either through the anonymity they provide or by the halo of legitimacy conferred by an app and branded uniforms/supplies.

“If I told my family about my work without the app, there would be a problem. I have a uniform and the bag, so they can see how my business is going. Transparency is good.”

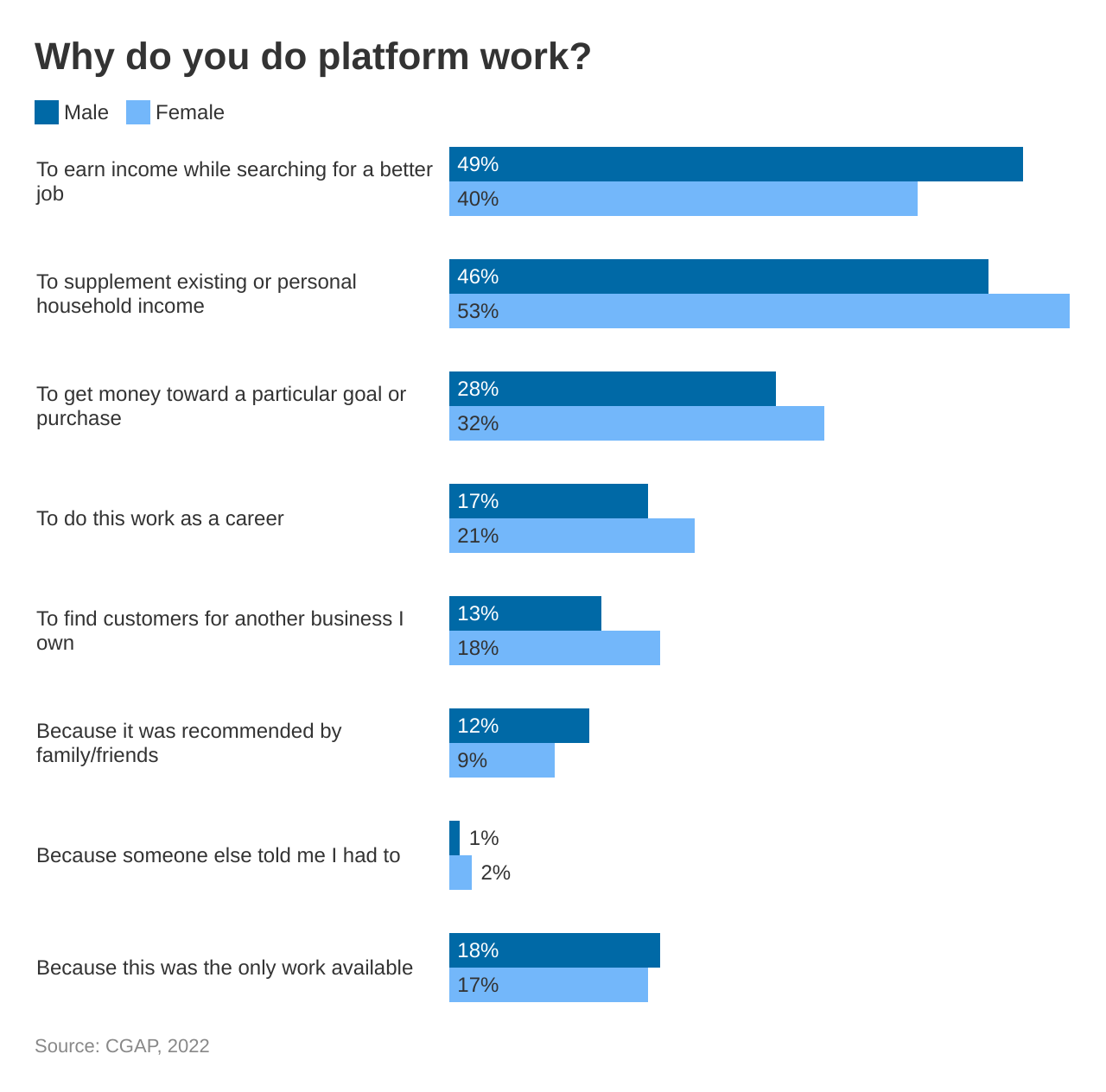

The flexibility of platform work allows women to consider it as a career path for better income-generating opportunities

The reported economic improvements came about despite the fact that most women work on platforms only part-time. At the same time, more women than men reported pursuing platform work as a career, and fewer report looking for other work. In fact, it may be due to its conduciveness to part-time work that so many women – who often balance paid work with significant labor within the home – saw platforms as a long-term part of their livelihood strategies. As one house cleaner on a platform in Indonesia explained, “It is just great when I can turn on the app and work. As a housewife, I can now make my own money and not have to ask my husband for an income.”

But women on platforms remain concentrated in “female sectors” and many challenges of offline work carry over

Despite these positive outcomes, many of the challenges women face in the offline work world persist on platforms. Most glaringly, women are still concentrated in “women’s work” sectors since platforms don’t have a major impact on the normative and structural forces that channel women into certain occupations over others. Work/life balance also remains a challenge, with almost a third of the women we spoke with reporting feeling pressured to spend less time on platform work so they could prioritize household and care responsibilities.

And while the women we consulted felt that online work was safer than offline, it’s still not safe enough: approximately 40% of women we surveyed agreed with the statements “Platforms do not protect me” and “The work environment is unsafe” (as opposed to 30% of men respondents). But the greatest difference – 45% of women vs. 32% of men – was in those who agreed that “The work is too mentally and physically demanding.”

“Once you're online, you can't go offline… You signed a contract that says you have to knock off at 10 o'clock so you have to do that. It's like any other job…If I could, I would ask for flexible hours. Only that. Maybe to rest a little bit.”

Women are keen to translate increased income from platforms into economic security but need additional financial tools

We also noticed signs of a disconnect between the increased income reported by women and their ability to translate that income into economic security. For example, while 20% more women than men said their per-job income had increased since starting platform work, more men said platforms had made it easier to meet daily expenses. Similarly, 50% more men than women said platform work had made it easier to set and achieve financial goals, while more women said they either save less or the same as before they started working on platforms.

However, our research indicated that women platform workers are hungry to translate their platform income into long-term economic gains. Compared to men, more women expressed interest in translating platform work into long-term security for their families; twice as many reported accessing insurance products since starting on platforms, and almost 50% more women than men said they would want life insurance if offered through platforms. Women’s income growth on platforms was also disproportionately constrained by lack of expansion capital. This suggests some clear use cases for financial services, including insurance, long-term savings and loans. Women also evinced a desire for financial planning assistance that would help them optimize their use of such offerings.

As critical as these elements are, though, it will take more than products and planning to bridge the divide between women increasing their income and using it to achieve economic goals. This disconnect often also has roots in the broad range of gender norms that come between women’s ability to earn and their ability to profit from those earnings, frequently manifested in intra-household dynamics around control over money and socially determined financial responsibilities.

To be able to realize their economic goals, women in platforms need bundled financial services rooted in an understanding of their daily lives

This is not to say that women’s social context is always negative: our research found that women’s networks were also key enablers of their success on platforms. Any product or service offering that aims to be gender-transformative must therefore take account of the diverse social contexts in which women operate. These and other insights from the research give rise to six specific recommendations for developing financial services for women platform workers, available with the complete findings:

-

Customize financial products and services to help women maximize the benefits of platform work for the long term.

-

Take note of women’s family obligations.

-

Bundle financial products with non-financial services to amplify their effectiveness.

-

Leverage women’s networks.

-

Tailor financial service offerings to the needs of specific sub-segments.

-

Ensure worker flexibility and design services to mitigate risks.

How well do current platform-mediated financial service offerings for women align with the implications of this research?

Full transparency: we weren’t able to find many examples of services aimed towards women working on platforms in our first round of supply-side research. That’s why we are undertaking a second round of research with expert partners to explore not only what financial service offerings are out there for women, but the different ways in which (quasi-)platformization (the increase in “near-platforms” like labor aggregators, benefits providers, and others) is changing the way workers can access such services in female-dominated sectors. This effort aims to address two key knowledge gaps we see.

First, we need a deeper understanding of the specific sectors within the platform economy where women are concentrated in order to identify entry points for designing financial services that enable greater economic opportunities. Examples include women selling products from home via social media platforms, or women providing domestic help through labor aggregators. Secondly, this understanding must be translated into truly women-centered financial service design across the platform ecosystem to ensure that offerings are rooted in the realities of women’s lives. Watch this space for the release of those findings later this year. In the meantime, join us online June 7, 2022, to learn more about the insights underpinning our recommendations and hear from platforms and fintechs seeking to leverage the potential of financial services for platform workers.

This blog is part of a broader CGAP effort over the coming months to work with platforms and financial services providers to pilot new financial solutions for this small but fast-growing segment of the economy that is transforming livelihoods opportunities for low-income communities. Visit www.cgap.org/platform-workers for more information and see our paper and reading deck for a deeper dive into the ideas introduced here.

")

")

Add new comment