|

Don’t Underestimate How Well Cash Works in Retail

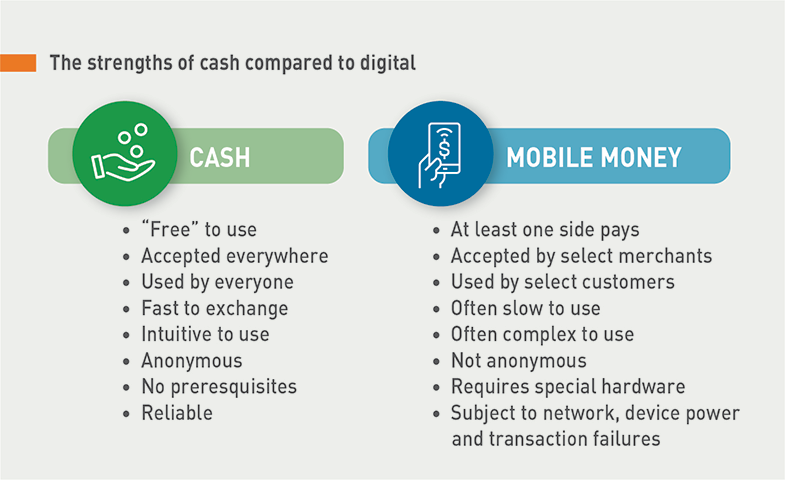

Many providers, even those in markets with high uptake of electronic wallets, have underestimated the strengths of cash when developing a merchant payments proposition. Cash is a system that has evolved over millennia, and its strengths reflect years of refinement. It is quick and intuitive, universally accepted, everyone knows how it works, and it doesn’t require electricity or network coverage.

The strengths of cash compared to digital

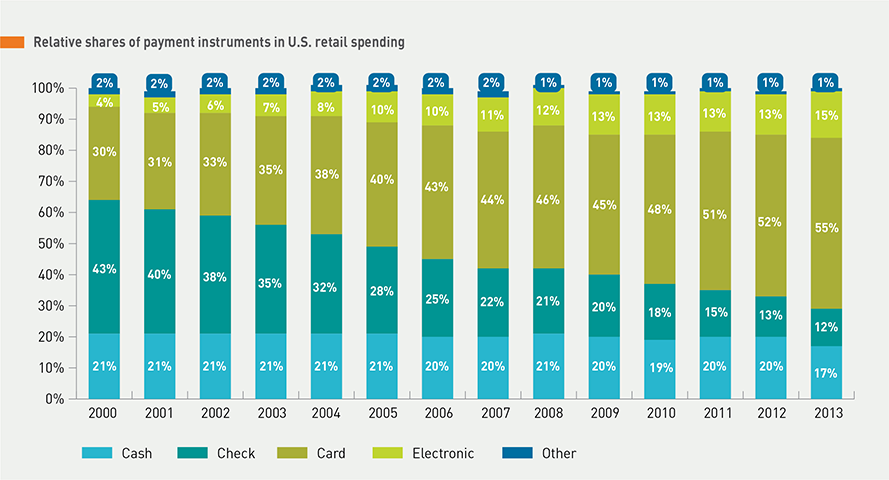

Even in advanced payments markets like the United States, cash use has not declined for over 15 years, even as card and electronic payments have grown rapidly. Instead, these forms of payment have displaced checks, while the use of cash has remained remarkably consistent.

Relative shares of payments instruments in U.S. retail spending

Don’t Overestimate the Appeal of Digital Payments

Early movers in the merchant payments space tended to assume that merchants and their customers will see digital payments as superior to cash. The pitch has typically revolved around ease and convenience, with the added benefits of security and a general notion that digital is always better. Unfortunately, for many merchants and their customers, this pitch hasn’t tended to resonate well with real-world circumstances.

While digital is arguably more secure—though there are important qualifications to that as well—and does have a cool factor for some people, the simple fact is that customers and merchants in developing economies tend to find cash to be more convenient than the first generation of mobile merchant payments solutions. While carrying cash does come with some inconveniences, until virtually all stores accept digital payments, people will still need cash, so a digital wallet does not actually free users from that.

Moreover, digital interfaces can also be inconvenient in that they are unfamiliar, can be complex, are often slow to use, and sometimes result in transaction failures and delays. Even if both parties prefer digital interfaces, platforms may not be interoperable; systems may be down; or devices may be broken, lost, or out of power.

In addition, merchants who do use the digital till to collect payments from their customers are often faced with a frustrating problem: the money is stuck there. The expenses they have, for example, for replenishing inventory and paying staff, are nearly always made in cash. Their suppliers don’t have digital wallets, and while their staff might have the wallets, they typically still prefer to be paid in cash. So now the merchant has to close the shop, find an agent, and pay a cash-out fee of several percent to get the cash back out. Accepting digital payments has created a new problem for merchants that they had not encountered with cash.

Hence the value of digital payments is not always as straightforward as providers assume. There are four critical dimensions in the competition between cash and digital in merchant payments: security, convenience, speed, and cost.

Security

Security is perhaps one of the easiest selling points of digital payments, since cash is vulnerable to things like theft, loss, and fire—and once gone, cash can’t be replaced. Digital payments have safeguards against loss (e.g., personal identity numbers [PINs]) and can usually be replaced if something goes wrong (e.g., a stolen phone or a lost SIM card). In some countries, such as in India, strong regulatory frameworks exist to protect users and can help guarantee the security of digital payments through insurance against fraudulent transactions.

Yet, in many developing counties, there are doubts about the perception and the reality of the digital world. When spotty connectivity leads to incomplete transactions or delays in confirmation messages, a level of uncertainty and insecurity is introduced. Policies about chargebacks and settlements can also disadvantage one party relative to the other. Fraud, identity theft, and mistakes when inputting numbers can also contribute to feelings of insecurity, undermining the security advantages of digital payments.

Convenience

The sheer simplicity of cash is one of its strongest selling points. Handing over a physical coin or bill is extremely intuitive, and even customers who are illiterate can generally differentiate between different denominations.

Digital payments systems require users to learn how to do something new. People are smart: after getting accustomed to digital interfaces and point-of-sale terminals, many find that they are not difficult to use. But the learning curve can be steep, and initially the systems can seem impenetrable. In many first-generation merchant payment implementations, conducting a transaction involves six or seven steps in a USSD menu, with menu options that are far from clear, even to educated customers. If such processes are too difficult, people won’t use the system enough to become familiar with it, and the product will fail.

In the context of mobile money agents, the shopkeeper herself has served as a resource to help people learn how to use their phone, set up a mobile money account, and execute operations. In the case of merchant payments, however, customers may be less inclined to depend on the shopkeeper for support since she is the one getting paid, and hence there is a potential conflict of interest.

For merchants, the usability of the funds collected in the account is critical. If they perceive that digital funds are stuck in the wrong place and are costly or time consuming to retrieve, they will not use the system. To maximize usefulness, providers should ensure that merchants can easily pay their suppliers directly from the digital wallet, settle out to a bank account in real time whenever they want, and cash out at no or little cost.

Speed

Cash transactions can be very quick, especially if change and receipts are not required. Customers have low tolerance for long lines and get irritated if a payment method is causing delays at the till. Digital payments can take a longer time to complete, especially if there are menus to navigate or data to enter by either customer or merchant, which is a drawback of many digital payment systems.

Choosing the right acceptance technology, which is discussed in “Acceptance Technologies for Merchant Payments,” is critical to meeting users’ expectations about speed at till. Some options, like near-field communication (NFC) or quick response (QR) codes, are much faster and less cumbersome than the USSD technology used by many first-generation merchant payments implementations. In China, mobile payments providers opted for QR codes, which are cheap to deploy and have led to a rapid displacement of cash in retail (for more information, see “China: A Digital Payments Revolution”). In Europe and the United States, NFC-based tap-and-go systems are increasingly prevalent, although they require specialized devices for both customer and merchant.

As users gain confidence using the system, transactions will be completed more quickly. In addition, better, quicker networks and terminals will increase speed. That said, in the interim, providers must ensure that speed of use remains a top priority when designing systems. Simple user interfaces and human-centered design can help improve speed as technology and devices improve.

It is worth noting that there is sometimes a trade-off between security and speed. PIN authentication and other measures can add time, but they increase security considerably. Confirmations can also take time, whether provided via printed receipt or SMS, especially when connectivity is poor. Improving the speed and streamlining these steps will help make digital payments more attractive.

Price

Cost is a critical weakness of digital payments in the contest with cash, for a simple reason: People almost universally think of cash as free to use. While there are significant costs of cash in the wider economy, cash does not come with transaction fees.

Digital payments, however, almost always do come with transaction fees, since that is the most obvious way to generate revenue from the service. Charging transaction fees is also the most problematic way to generate revenue, since it directly deters people from doing the very thing the entire business rides on: pay digitally. For more on this challenge for providers, see “Don’t Charge Transaction Fees.”

This does not mean, however, that digital payments can never compete with cash, even though they are not offered for free. It is a question of the balance between what you pay and what you get in return. Enticing merchants or customers to pay for a straight payments product is always going to be hard, as discussed in “If What You Are Selling Is a Solution to the Cash Problem, Don’t Bother.”

However, if providers offer compelling VAS around and on top of the payments piece, users will be happy to pay for those. Put differently, while the cost of digital payments is higher than that of cash, the value of the digital solution can be higher as well.

See “Choosing a Profit Strategy for Merchant Payments” for advice on how to minimize/eliminate fees while using VAS and other functionalities to earn revenue.

The Value of Digital Retail Payments Lies beyond the Payment Itself

Despite challenges that come with digital payments, providers should not conclude that there is no case for digital payments in retail—there absolutely is. After all, the total costs of cash in the economy are substantial: Visa estimates the cost of cash transactions in India to be 1.7 percent of gross domestic product. Conversely, digital merchant payments can open up excellent new opportunities for products and services that add value to users and generate revenue for providers.

The problem is that neither the costs nor the potential revenue gains accrue to the merchants and customers who make the critical decision about which payment instrument to use. They don’t see the costs of cash to society and are not taking them into account when making their decisions. Why should they? Hence the very people who have the power to choose whether the economy should switch away from cash have no real stake in that choice.

To gain traction, providers must realize the benefits of digitizing payments and distribute them to customers and merchants so as to align incentives in favor of digital payments. To get people to make the switch, providers should create an alternative product that has its own distinct benefits. If, for example, consumer goods companies can save costs and get valuable data by switching to digital payments in their distribution chains, they are also willing to pay for that. This revenue can be shared back to merchants and customers in various ways to give them a reason to choose digital payments.

For merchants, such revenues can be used to offset transaction fees and cash-out fees, which as discussed in “Transaction Fees,” are a considerable hurdle to uptake. Better yet, they can be leveraged to power a variety of VAS aimed at easing the pain points in merchants’ business and thereby make digital payments more attractive. For more about VAS and their role in creating compelling value for merchants, see “For Merchants, the Real Value Lies beyond Payments.”

For customers, loyalty models can drive use. They have been deployed successfully by the card industry for decades as a way to boost the value of plastic. Loyalty models can be used by digital payments players not only to incentivize end customers but also to strengthen engagement with the merchant network. See “Loyalty Models Can Create Value for Consumers.”

Crucially, these incentives need to be part of the value proposition from day one. Many providers foresee building additional services around and on top of digital payments products, but they plan to do it later, after they scale and become profitable. A critical caveat providers must take to heart is that, if they put off the parts of the product that genuinely add value to users, “later” most likely will never come.